Jump to:

8.1 Strengthen support for inclusive and sustainable economic recovery from COVID-19 8.2 Accelerate development of productive capabilities to drive structural transformation 8.3 Enhance trade linkages with the developing world 8.4 Deepen regional integration and improve regional connectivity to expand trade 8.5 Close digital divides within and between Commonwealth LDCs and other countries 8.6 Leverage digitalisation to boost trade, productive development and competitiveness 8.7 Prioritise provisions for smooth LDC graduation through multilateral commitments 8.8 Enhance debt sustainability and de-risk, incentivise and improve access to finance 8.9 Grow capacity to attract productive investment, including FDI and green investment 8.10 Support climate adaptation and resilience and natural disaster risk reduction

In many respects, the publication of this report comes at a watershed moment for LDCs. The COVID-19 pandemic has arrested their economic growth, stifled production, disrupted sectors of critical importance (especially tourism, textiles and readymade garments) and stymied exports. These and other impacts threaten to raise poverty levels and widen existing inequalities within LDCs and between them and more developed countries, in the process reversing decades of economic and socio-economic development progress. As the search for a path out of the pandemic and the race to roll out vaccinations intensifies, albeit with significant and concerning disparities between LDCs and more advanced developing and developed nations, LDCs and their development partners need to develop innovative policies, programmes and strategies to facilitate sustainable and inclusive recovery.

It is also necessary to look beyond the COVID-19 pandemic to craft a new programme of action to drive forward LDC development over the next decade. This requires both reflection on the achievements, challenges and learnings from the past decade of IPoA implementation and consideration of how a new programme of action can better address the contemporary constraints to economic and social transformation facing LDCs. Renewed efforts are required to confront the multiple challenges hindering growth in trade, productive development, structural transformation and poverty alleviation, many of which have been exacerbated by the COVID-19 pandemic.

Those tasked with addressing these challenges will need to be cognisant of several continuing and newly emerging trends within the global economy that will influence the economic development trajectory of LDCs over the coming decade. Among these, rapid digitalisation of economies, societies and work, along with exponential growth of the digital economy, point to an increasingly digital future. These trends have accelerated with the onset of the COVID-19 pandemic, fuelling growth in digital trade, especially e-commerce, and highlighting the importance of digital transformation. With limited digital connectivity, shortcomings in digital infrastructure, low levels of digital capacity and skills, and underdeveloped regulatory environments, many Commonwealth LDCs are poorly positioned to benefit from the opportunities available in the digital economy. Addressing these shortcomings is critically important if LDCs are to narrow existing digital divides and, in the process, prevent further marginalisation in an increasingly digitalised global economy.

Similarly, the rapid development and deployment of new “frontier technologies” – a feature of the Fourth Industrial Revolution (or Industry 4.0) – holds considerable potential to help drive economic recovery and spearhead economic transformation (UNCTAD, 2021b). However, an inability to harness and adopt these technologies means many LDCs face the risk of being left behind (Commonwealth Secretariat, 2021). Rapid advances in automation, robotics and 3D printing are likely to reduce demand for traditionally manufactured goods and undermine their competitiveness, with significant implications for manufacturing, jobs and livelihoods in more technologically constrained countries. Large investments in digitalisation will be required to develop the digital infrastructure, capabilities and skills necessary for LDCs to use, adopt and adapt frontier technologies effectively.

Broader structural shifts are also underway within GVCs, with implications for Commonwealth LDCs, especially countries such as Bangladesh, Lesotho and Tanzania, which possess relatively more developed export-oriented manufacturing capacity. Even prior to the emergence of COVID-19, greater emphasis on re-shoring and regionalisation, as well as a pivot in focus to regional market-seeking FDI and shorter value chains, was changing the dynamics of global manufacturing. The pandemic has reinforced some of these shifts, heightening the focus on restructuring GVCs to de-risk and build resilience to future crises. Most Commonwealth LDCs are located far from international production centres, thus undermining prospects for producers in these countries to engage in GVC-intensive manufacturing and export industries in an environment in which near-shoring, re-shoring and regionalisation are increasingly favoured.

These shifts are also influencing prospects for attracting investment. Increased divestment, investment diversion and changes in the key locational determinants of investment, as well as a generally shrinking pool of efficiency-seeking investment, mean Commonwealth LDCs are likely to face even greater competition to attract FDI inflows going forward (UNCTAD, 2020a; Commonwealth Secretariat, 2021). More focus on environmental, social and governance considerations in FDI decisions is also reshaping the vectors of competitiveness for countries looking to attract investment. Nevertheless, some Commonwealth LDCs may be well positioned to attract investors looking to diversify supply bases and increasingly prioritising market-seeking FDI (East and Kaspar, 2020; UNCTAD, 2020a). This is particularly promising for African LDCs benefiting from low costs and relatively large markets, which have expanded with the regional trade and investment opportunities arising from the African Continental Free Trade Area (AfCFTA).

For commodity-dependent Commonwealth LDCs, the prospect of a new commodity super cycle bodes well for a rapid recovery in commodities trade after the collapse in prices of many commodities witnessed in the first half of 2020. Supply constraints in 2020, many of which continued into 2021, alongside recovering demand, pushed up prices of commodities such as copper, grain, iron ore, liquified natural gas, pork, soybeans and wheat (The Economist, 2021). Oil prices have also recovered after plummeting in 2020 as the economic fallout from the COVID-19 pandemic intensified. A surge in prices of most commodities since the second half of 2020 should help commodity-dependent Commonwealth LDCs to offset some of the trade loses suffered as a result of the pandemic and recover from some of its real economy consequences.

Recognising these trends, and considering the evidence presented in the previous chapters, a 10-point action plan is set out below and summarised in Table 23, highlighting priorities to address the special needs of Commonwealth LDCs and improve their trade and development prospects. These priorities are intended to help guide discussions towards an ambitious new programme of action for LDCs spanning the decade 2022-2031.

8.1 Strengthen support for Commonwealth LDCs to achieve inclusive and sustainable economic recovery from COVID-19

The analysis in Chapter 5 shows that COVID-19 has slowed growth; increased unemployment; led to significant losses in working hours, productivity and sectoral value added; stifled trade; and severely constrained finance, ODA and investment flows to Commonwealth LDCs, even though these countries have generally been more resilient than many of their non-Commonwealth counterparts. If they persist, these adverse impacts threaten to reverse developmental gains made over the past few decades. A protracted pandemic also poses significant risks to sustainable graduation pathways for Commonwealth LDCs. LDC governments, with their development partners, will need to accelerate efforts to eliminate existing vulnerabilities and build greater resilience if they are to effectively confront the heightened challenges emanating from COVID-19 (Commonwealth Secretariat, 2021).

In the short term, a major priority should be to ensure more equitable and affordable access to vaccines in Commonwealth LDCs. This is an essential step to kick-start economic activity and get key sectors such as tourism back on track. If the stark inequalities in vaccine access and distribution between developed and developing countries persist, LDCs – which generally have among the lowest vaccination rates – risk being left behind. Greater financial support for LDCs to procure vaccines along with other medicines and diagnostics, backed by reduced vaccine costs, would help address inequalities in access. At the same time, greater international co-operation is necessary to scale up the distribution of COVID-19 vaccines to LDCs, including by leveraging existing multilateral arrangements and agreements such as the World Health Organization’s COVAX Facility and Access to COVID-19 Tools Accelerator and the United Nations Technology Bank’s Technology Access Partnership for LDCs.

A negotiated outcome to the proposed general waiver to the TRIPS Agreement for drugs, vaccines, diagnostics and other technologies related to COVID-19 would broaden the number of countries producing, developing and exporting generic vaccines and help scale up production to meet global demand. However, some countries argue that the Doha Declaration on TRIPS and Public Health already provides sufficient flexibilities to strike the right balance between safeguarding intellectual property holders’ rights and public health considerations (Vickers et al., 2021b). Stronger regional co-operation – building, for example, on existing initiatives such as the Africa Centres for Disease Control and Prevention’s Africa Medical Supply Platform – can also enhance the procurement and distribution of vaccines to LDCs, alongside national allocation frameworks and distribution plans supported by the private sector.

In the longer term, LDCs should look to redouble efforts to develop productive capabilities and target investments in key productive sectors. They also need to build capacity to grow and diversify exports and take advantage of the tariff preferences offered by developed countries, such as the EU’s Everything But Arms scheme, and some developing economies, especially China and India. One option in this regard would be to extend preferential schemes for LDC exports to include duty-free access for LDC value added embodied in third country exports of finished products (Cernat and Antimiani, 2021). Under such a scheme, LDC exports would enjoy duty-free access across GVCs. This could boost their exports, assist them to integrate into GVCs and enable them to participate more effectively in global trade, while also helping diversify their production and export bases by supplying intermediate inputs in a wider range of sectors (ibid.).

Expanding LDCs’ digital economies and bridging digital divides should also be a priority amid the surge in digitalisation globally, along with greater attention on climate adaptation and resilience and natural disaster risk reduction. These and other priorities are outlined in the remaining action points and will be key to charting a path towards a more inclusive and sustainable recovery from the pandemic.

8.2 Accelerate the development of productive capabilities in Commonwealth LDCs to drive structural transformation

Successive programmes of action have placed increasing emphasis on boosting the productive capacity of LDCs. Even though Commonwealth LDCs have made some advances in diversifying their economic bases and building productive capabilities (see Chapter 2), persistent constraints continue to stall progress in achieving the economic transformation necessary to generate a step-change to a more sustainable growth path. A multi-pronged approach is necessary to accelerate the development of productive capabilities in higher-productivity sectors and higher-value added activities in Commonwealth LDCs to reach a level necessary to meaningfully transform their economies and make them more resilient to future shocks.

Better access to new technologies in Commonwealth LDCs, backed by enhanced capabilities for innovation, can play a catalytic role in raising productivity and supporting more advanced production focused around more complex and differentiated products and services. In the agriculture sector, for instance, digitalisation and the use of innovative technologies can enhance yields and productivity, accelerate value addition and help diversify production (ECOSOC, 2021a; UN-OHRLLS, 2021). Similarly, Commonwealth LDCs possessing relatively more established industrial sectors – such as Bangladesh, Lesotho, Mozambique and Tanzania – can look to harness new technologies in order to produce more complex and differentiated products. Digital technologies can also aid the delivery of more advanced and higher-value added services both within Commonwealth LDCs and for export to other markets. With these opportunities in mind, the United Nations Technology Bank for LDCs should be strengthened to better support access to technologies, including by facilitating technology transfer and assisting LDCs to adopt and adapt new technologies for local settings. Significant increases in investment – alongside dedicated policies – are also required to develop their capabilities in science, technology and innovation.

A step-change is necessary in the level of financial resources available to Commonwealth LDCs for productive development. Beyond managing debt-related inflows and attracting FDI (discussed in Sections 8.8 and 8.9, respectively), Commonwealth LDCs can also look to deploy remittances as a development resource to enhance productive capacity. Remittances are a major source of financial inflows to LDCs, and generally expanded in Commonwealth LDCs across the IPoA period, notwithstanding the decline in 2020 caused by the COVID-19 pandemic. However, as Chapter 4 explained, they have historically been directed towards current household consumption in LDCs rather than financing investment in productive activities.

Commonwealth LDCs can also build productive capabilities in the private sector by upgrading and diversifying the domestic enterprise base. This requires interventions to develop human capital and improve access to finance. The latter can be supported through credit guarantee schemes and incentives for banks to provide dedicated financing to MSMEs (UN-OHRLLS, 2021). Development partners can also help broaden access to finance by providing concessional finance for start-up businesses in LDCs.[1] Finally, strategically attracting FDI (discussed further in Section 8.9) to develop linkages with local enterprises and transfer skills and technology can help expand capabilities in the domestic private sector.

8.3 Enhance trade linkages with the developing world

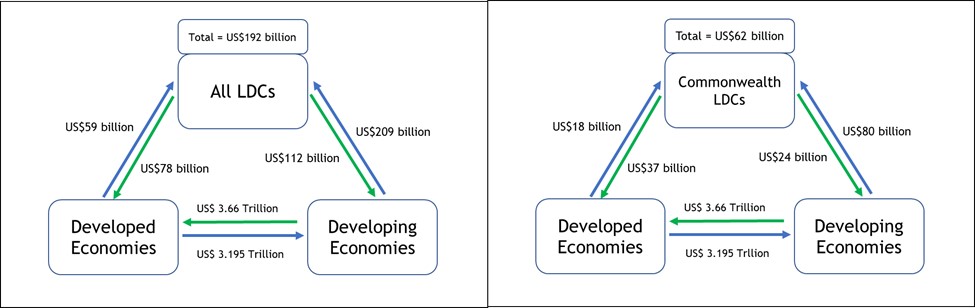

One of the major developments in the world economy over the past three decades has been the rapidly growing share of developing countries in world trade. A related trend is LDCs’ increasing economic engagement with developing economies. In 2019, their merchandise trade flows (exports plus imports) with developing countries was worth US$321 billion, more than double their trade ($107 billion) with developed economies (Figure 45). Similarly, Commonwealth LDCs’ trade with the developing world ($104 billion) was worth almost double their trade with developed economies ($55 billion).

This shift in trade orientation is evident in both exports and imports. In 2019, all 47 LDCs sent around two-thirds of their exports to developing countries and sourced around four-fifths of their imports from them. The 14 Commonwealth LDCs exhibited similar trade patterns: they sourced more than three-quarters of their imports from developing countries and sent around half of their merchandise exports to those markets.

Figure 45: Orientation of LDCs’ merchandise trade in 2019

These expanding trade linkages with the developing world offer a great opportunity for a quick rebound in LDC exports because most developing regions are predicted to grow faster than the developed world. Two large developing economies, India and China, offer tariff preferences and other support measures to boost LDC trade. China’s programme, for instance, provides for considerable economic, industry and investment co-operation with LDCs. It also helps LDCs increase trade with developing countries as well as with other LDCs by supporting them to build capacity to engage in trade negotiations and participate effectively in WTO activities.[2] The recent South-South dialogue on LDCs and development, the fourth in this series sponsored by China, was held in Geneva in September 2021.

8.4 Deepen regional integration and improve regional connectivity to expand trade in Commonwealth LDCs

All Commonwealth LDCs are located in extremely dynamic regions of the world economy, where regional trade and investment initiatives are gearing up under the auspices of mega regional trade blocs. For instance, there are nine Commonwealth LDCs in Africa, where trading under the AfCFTA started in early 2021. Similarly, the four Commonwealth LDCs in the Pacific are at the periphery of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership and the Regional Comprehensive Economic Partnership (RCEP) in Asia-Pacific, which is expected to be operational from 1 January 2022. Active engagement in these regional trade agreements could offer numerous opportunities to attract investment and participate in regional and global value chains.[3]

Commonwealth LDCs will need to accelerate their efforts to address logistical constraints and improve trade connectivity infrastructure if they are to capitalise on these opportunities over the next decade. The critical role of logistics services in facilitating trade and economic development cannot be overemphasised. Roughly half of world trade is organised around regional and global value chains, and logistics services are the “glue” that holds these value chains together. A country's trade competitiveness correlates closely with its logistics performance, which relies not only on hard infrastructure, such as ports and road networks, but also on the ability to supply cost-effective logistics services. This is particularly important for the landlocked Commonwealth LDCs in Africa (Lesotho, Malawi, Rwanda, Uganda and Zambia).

8.5 Close digital divides within Commonwealth LDCs and between them and other countries

Despite progress in expanding access to the internet, along with some improvements to internet bandwidth, Commonwealth LDCs are still plagued by low levels of internet penetration and poor network connectivity linked to inadequate digital infrastructure and high ICT costs. These factors, along with limited digital skills and capabilities, are widening digital divides both within LDCs and between LDCs and their more developed counterparts.

A broad range of interventions are necessary to close these divides and enhance digital engagement in Commonwealth LDCs. Specific attention should be accorded to improving digital literacy by investing in digital education and skills development, promoting digital connectivity and developing digital infrastructure. This can be delivered through partnerships and co-operation between the public and the private sectors in LDCs, supported by civil society organisations, development partners and international institutions.

There is an urgent need to ensure the internet and other ICTs are more accessible and affordable in Commonwealth LDCs. The Broadband Commission for Sustainable Development has set a target of ensuring entry-level broadband services cost less than 2 per cent of monthly GNI per capita in LDCs. Most Commonwealth LDCs will require significant improvements to their digital infrastructure to reach this goal. Specific interventions at the national level to expand the roll-out of fibre optic cables and extend mobile broadband services can help bring down prices and boost internet usage (UN-OHRLLS, 2020). These will need to be backed by improvements to the regulatory frameworks governing markets for ICT infrastructure and services in Commonwealth LDCs.

8.6 Leverage digital technologies to boost trade, productive development and competitiveness in Commonwealth LDCs

Digital technologies and digital trade (including e-commerce) can help raise productivity, enable more advanced and diversified production, support better and more sustainable integration into supply chains, and expand and diversify LDC exports. Rwanda’s ambitious digitally led development model provides an inspiring example of how prioritising a digitalisation agenda can help overcome the connectivity constraints associated with being landlocked and provide a base from which to accelerate economic transformation (Commonwealth Secretariat, 2021).

Rapid technological advances and new frontier technologies linked to Industry 4.0 offer great promise to help drive economic recovery from the COVID-19 pandemic and spearhead longer-term economic transformations. By harnessing these and other digital technologies, LDCs can also build greater resilience to future shocks.

However, Commonwealth LDCs generally remain constrained by their lack of capacity to leverage digital technologies effectively. As with efforts to narrow digital divides (see Section 8.5), addressing these shortcomings will require significant investments to build their digital capabilities, develop digital infrastructure, and upskill and train their workforces with new digital skills. Special attention needs to be directed to empowering MSMEs, along with women and youths, to access and engage with digital technologies. Moreover, approaches aimed at developing science, technology and innovation capabilities in LDCs need to be better aligned with these countries’ broader industrial policies and their strategies for achieving inclusive and sustainable economic transformation.

A newly invigorated Aid for Digital Trade initiative would help direct more donor support to enhance the participation of LDCs in digital trade (Commonwealth Secretariat, 2021). As suggested by Lacey (2021), such an initiative could focus initially on:

- Developing digital infrastructure;

- Empowering individuals, consumers, entrepreneurs and businesses with the skills necessary to adopt and utilise digital technologies;

- Funding to support the development and roll-out of digital government services as well as to enable the adoption of digital and online systems; and

- Enabling access to financial services and broadening financial inclusion, including through FinTech and digital financial services.

However, to maximise the impact of this support and avoid simply reallocating existing aid resources that are sorely needed elsewhere, donors must ensure that any Aid for Digital Trade is provided to LDCs in addition to existing ODA and Aid for Trade flows.

8.7 Prioritise provisions for a smooth transition process for graduating LDCs through multilateral commitments

The dawn of a new programme of action presents an opportunity to renew and strengthen international support measures aimed at developing sustainable graduation pathways for LDCs. The multilateral trading system will continue to have an important role to play in this regard, particularly by supporting LDCs to develop productive capacities and diversify their economies through trade. Special measures are required to lessen their dependence on exports of commodities and low-value added products and services.

LDCs’ trading partners can support their smooth transition out of the LDC category by sustaining preferences and committing to provide technical assistance and capacity-building support after they graduate. An extension of unilateral market access schemes for graduated LDCs for 12 years after their effective date of graduation, as proposed by the LDC Group, would provide a crucial step in this direction, and could be accompanied by a work programme to agree on an appropriate period for phasing out these schemes for graduated LDCs.[4]

These commitments should be accompanied by greater access to concessionary borrowing through multilateral development banks and progressive debt relief for LDCs – as argued below – to enable them to channel resources to development projects that support graduation and enable post-graduation sustainability.

8.8 Enhance debt sustainability and de-risk, incentivise and improve access to finance for Commonwealth LDCs

COVID-19 has worsened the tenuous fiscal position of some Commonwealth LDCs. The pandemic has severely constrained finance and investment flows globally and curtailed inflows of external finance, with significant implications for those countries that were already reeling from declining ODA inflows, rising levels of external debt and concerns over debt sustainability during the IPoA (see Chapters 4 and 5). Moreover, the pre-existing fiscal constraints in many LDCs, which have worsened since the emergence of COVID-19, have severely hampered their ability to mount a fiscal response. In the wake of heightened uncertainty around future ODA and dwindling inflows of other financial resources, levels of external debt – which were already alarmingly high in many African Commonwealth LDCs – have risen markedly. This has been compounded by rapid increases in the cost of non-concessional borrowing since the beginning of 2020.

To deal with these challenges, Commonwealth LDCs – and indeed the LDC group as a whole – require more concerted and targeted debt relief. A longer extension to the moratorium on debt servicing through the G20-led Debt Service Suspension Initiative would provide some relief, especially if it were extended to include private creditors. Continued preferential access for LDCs to concessional finance would provide further relief (UNESCAP, 2021). Commonwealth LDCs would also benefit from support from multilateral institutions to facilitate debt restructuring.

Looking further ahead, a priority for Commonwealth LDCs should be to ensure that their interests are adequately reflected in the ongoing discussions to reform the global financial architecture. This is especially important in relation to discussions on revisions to the debt sustainability framework to ensure it aligns better with the SDGs, the provision of technical assistance to strengthen debt management and the establishment of effective systems for repaying external debt (UNCTAD, 2021c).

Commonwealth LDCs can also lobby for a reallocation of Special Drawing Rights (SDRs) away from countries that do not utilise them and in favour of those facing liquidity challenges. The quotas currently available to LDCs fall well short of their needs, yet unused SDRs total nearly US$130 billon globally. Better utilisation of these resources through a reallocation of quotas would help address this imbalance.

Importantly, Commonwealth LDCs should push to ensure any reallocation of SDRs does not come at the expense of ODA disbursements. A renewed commitment by donors to fulfil their ODA obligations should form a fundamental pillar of any new programme of action for the next decade. The restoration of ODA levels to the targets endorsed by the 2030 Agenda for Sustainable Development – in which DAC donors committed to providing between 0.15 and 0.2 per cent of GNI to LDCs in the form of ODA[5] – is critically important to support the sustainable development of LDCs.

This also needs to be backed by efforts to ensure Commonwealth LDCs are better equipped to mobilise and retain domestic financial resources over the next decade. These should include targeted support to improve systems for tax administration. Depending on the specific needs of individual Commonwealth LDCs, such support could encompass assistance with tax policy design, support for public financial management and planning, or help to strengthen their capacity to combat illicit financial flows (UNCTAD, 2021c).

8.9 Grow the capacity of Commonwealth LDCs to attract productive investment, including FDI and green investment

FDI can make a significant contribution to growth, development and prosperity by transferring technology and skills, creating jobs, building productive capacity and making it easier for domestic firms to integrate into international production networks and access foreign markets. It often plays an especially important role in LDCs, where stocks of domestic capital and savings tend to be insufficient to finance productive investments. Despite these potential benefits, Chapter 4 shows that net FDI inflows generally followed a downward trajectory in most Commonwealth LDCs during the IPoA implementation period. Moreover, the vast majority of announced greenfield FDI – which can be instrumental in enhancing productive capacity and creating jobs – was concentrated in only four Commonwealth LDCs: Bangladesh, Mozambique, Tanzania and Zambia. To make matters worse, FDI inflows to most Commonwealth LDCs were badly affected by COVID-19 and fell short of pre-pandemic averages (see Chapter 5).

With these difficulties in mind, any new programme of action for Commonwealth LDCs should accord priority to strengthening measures to promote investment. Specific support measures could range from investment guarantees or risk insurance schemes to capacity-building for investment promotion agencies (UN-OHRLLS, 2021).

This should be accompanied by renewed emphasis on mobilising FDI into key productive sectors. Investments supporting the development of productive capital should be prioritised and incentivised, especially those bringing new technologies to upgrade existing sectors or diversify the economic base (Commonwealth Secretariat, 2021). FDI can also be harnessed to develop export capacity, provided it is accompanied by trade promotion policies to generate a supply response (ibid.).

Commonwealth LDCs should look to attract more investment into key areas likely to underpin future growth, such as digital sectors and those supporting the green transition. Large investments in greener and digital technologies are required to facilitate a sustainable economic recovery from the COVID-19 pandemic, revive trade and build resilience. Investments in the renewable energy sector need to be prioritised. The shift to renewables is important as exports from some LDCs, such as aluminium produced in Mozambique, are at risk of facing additional barriers as a result of the potential carbon pricing mechanisms under development in the EU, Japan, the USA and Canada (Vickers et al., 2021a). LDCs exposed to carbon border adjustment mechanisms would need enhanced access to cleaner production technologies to shift away from existing energy-intensive manufacturing techniques.

8.10 Expand resources and support for climate adaptation and resilience and natural disaster risk reduction in Commonwealth LDCs

LDCs, especially low-income SIDS, are most vulnerable to the physical effects of climate change, despite having contributed the least to global warming. LDCs that have graduated or are graduating continue to confront this reality too. These countries need substantial support from the international community to adapt to climate change and build resilience to a future where the economic and human devastation that recurrent natural disasters have wrought is expected to increase in frequency and severity because of climate change, population growth and urbanisation.

Support for climate change adaptation, including finance, technology transfer and capacity-building, is well established under the United Nations Framework Convention for Climate Change, especially the Paris Agreement, and was reaffirmed at the 26th Conference of the Parties held in Glasgow in 2021. Development partners should implement their commitments and provide support for LDCs to develop national adaptation plans. This includes adequately resourcing and replenishing the LDCF and reducing the administrative burden to ensure easier access to climate financing.

LDCs and development partners should harness Aid for Trade to build robust trade-related infrastructure and enhance productive capacity, which will contribute to greater resilience in the wake of disasters. Furthermore, development partners should mobilise public and private investment in LDCs, especially to support greener production and a just transition to a lower-carbon economy.

Over the decade of the IPoA, the global community commendably supported disaster-hit LDCs with relief, recovery and resilience efforts. Given that these catastrophes are expected to increase in the future, the new programme of action should reaffirm this commitment by providing adequate financing and capacity support for LDCs to develop plans for disaster risk reduction, emergency preparedness and post-disaster reconstruction efforts in line with the Sendai Framework for Disaster Risk Reduction (2015–2030).

Table 23: Commonwealth 10-point programme of action for LDCs in summary

|

Action |

Priorities |

|

Strengthen support for Commonwealth LDCs to achieve inclusive and sustainable economic recovery from COVID-19 |

|

|

Accelerate the development of productive capabilities in Commonwealth LDCs to drive structural transformation |

|

|

Enhance trade linkages with the developing world |

|

|

Deepen regional integration and improve regional connectivity to expand trade in Commonwealth LDCs |

|

|

Close digital divides within Commonwealth LDCs and between them and other countries |

|

|

Leverage digital technologies to boost trade, productive development and competitiveness in Commonwealth LDCs |

|

|

Prioritise provisions for a smooth transition process for graduating LDCs through multilateral commitments |

|

|

Enhance debt sustainability and de-risk, incentivise and improve access to finance for Commonwealth LDCs |

|

|

Grow the capacity of Commonwealth LDCs to attract productive investment, including FDI and green investment |

|

|

Expand resources and support for climate adaptation and resilience and natural disaster mitigation in Commonwealth LDCs |

|

[1] As highlighted in the Political Declaration stemming from the Africa Regional Review Meeting held in preparation for LDC5 in Lilongwe, Malawi, 22-26 February 2021.

[2] https://www.wto.org/english/thewto_e/acc_e/china_programme_e.htm

[3] To join the RCEP, for instance, Commonwealth LDCs would have to replicate the approach taken by three non-Commonwealth LDCs – Myanmar, Lao People’s Democratic Republic and Cambodia – which are members of the trade agreement (see https://oecd-development-matters.org/2021/01/29/regional-comprehensive-economic-partnership-why-should-it-involve-the-excluded-ldcs/ for a detailed discussion). The RCEP’s flexible schedule of tariffs and long transition period are likely to suit most Commonwealth LDCs. Even without joining the trade bloc, Commonwealth LDCs can still benefit from the trade preferences of five RCEP countries – Australia, China, Japan, South Korea and Thailand.

[4] The LDC Group also proposed an interim arrangement for smooth transition by requesting WTO members granting LDCs unilateral trade preferences to put procedures in place to extend and gradually phase out their preferential market access schemes for graduated countries over a period of six to nine years.

[5] This is in parallel to a commitment to provide the equivalent of 0.7 per cent of GNI in ODA to developing countries.