3. Commonwealth Asia

3.1 Overview of agriculture in Commonwealth Asia

Of the eight (8)Commonwealth member countries in Asia, five (5) are classified by the United Nations Statistics Division as South-Asian countries. The other three (3) are in the South-East Asian region.

Below is a summary of characteristics of agriculture in Commonwealth Asia

- The agriculture, forestry and fishing sector contribute an average of 11.07 per cent to the GDP of Commonwealth Asia and employs 22.15 per cent of the population.[1]

- Agricultural land makes up 36.2 per cent of the total land area and 25.47 per cent of the land is arable.

- The rural population plays a major role in agricultural activities in the Asian Commonwealth with 53.01 per cent of the total population residing in rural areas.

- The Asian continent is an important global food hub. It accounts for 19 per cent of the global food and agricultural exports and 31 per cent of imports.[2]

- Approximately 90 per cent of the world’s rice supply emanates from Asia.[3] In countries such as Pakistan, Central Asia and Malaysia, rice fields cover more land than any other crop grown.

- Most farms in the Asian Commonwealth countries are smallholder in nature with an average farm size of 1.8 hectares.[4]

3.2 Systemic constraints to agriculture in Commonwealth Asia

3.2.1 Climate vulnerability and agriculture productivity

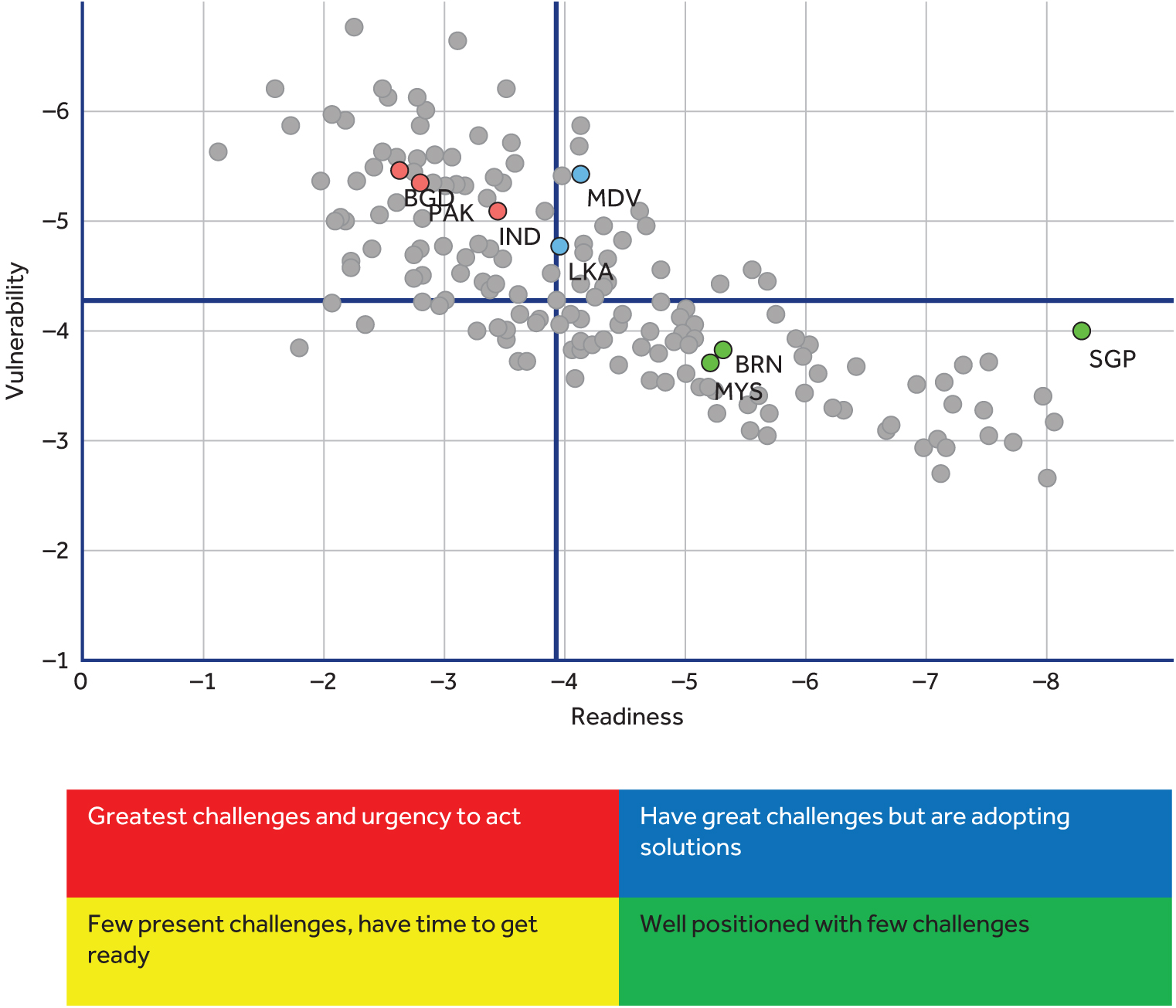

The level of climate vulnerability and readiness varies for the different Asian countries in the Commonwealth. Bangladesh, Pakistan and India are three of the eight Commonwealth countries in Asia with a high level of vulnerability to climate change, but a low level of readiness. These countries have a great need for investment to improve readiness and a great urgency for adaptation action.

- In Bangladesh, erratic rainfall, temperature extremes, increased salinity, droughts, floods, river erosion, and tropical storms are adversely affecting agriculture. Incidences of floods, droughts and high temperatures are predicted to become more frequent and intense in the future. These changes could lead to falls in crop yields of up to 30 per cent, creating a very high risk of famine.[5]

- In Pakistan, the increased variability of monsoons, likely impact of receding Himalayan glaciers on the Indus River system, decreased capacity of water reservoirs, reduced hydropower during drought years, and extreme events including floods and droughts are adversely affecting agriculture.[6]

- In India, rise in average temperatures, changes in rainfall patterns, increasing frequency of extreme weather events such as severe droughts and floods and the shifting of agricultural seasons have been observed in different agro-ecological zones of the country.[7]

The effects of climate change in the most vulnerable countries are being felt more adversely by smallholder farmers than by bigger and more established famers. This is because smallholder farmers do not have the adaptive capacity to cope with the effects of climate change.

Source: Notre Dame Global Adaption Index, 2017

Climate change in the region is having adverse effects on agriculture productivity. For example, the changing rainfall patterns affect the sowing period, productivity and product pricing. Additionally, changing and untimely rainfall patterns typically lead to an infestation of diseases and weeds that farmers are unable to manage. This in turn has a negative impact on productivity. When productivity gets affected, out of desperation, farmers react by using more inputs (fertilisers) and growth promoters (newly emerging) to ensure the desired level of output. This increases the cost of production as farmers are spending more on inputs. Such expenditures affect farmer margins.

To show the level of vulnerability to climate shocks and readiness to respond to these shocks, the ND-GAIN Matrix is used. The Matrix provides a visual tool for quickly comparing the current state of climate vulnerability and readiness of different countries (Figure 3.2).[8]

3.2.2 Access to finance and investment

Current state of financing and investment to smallholders

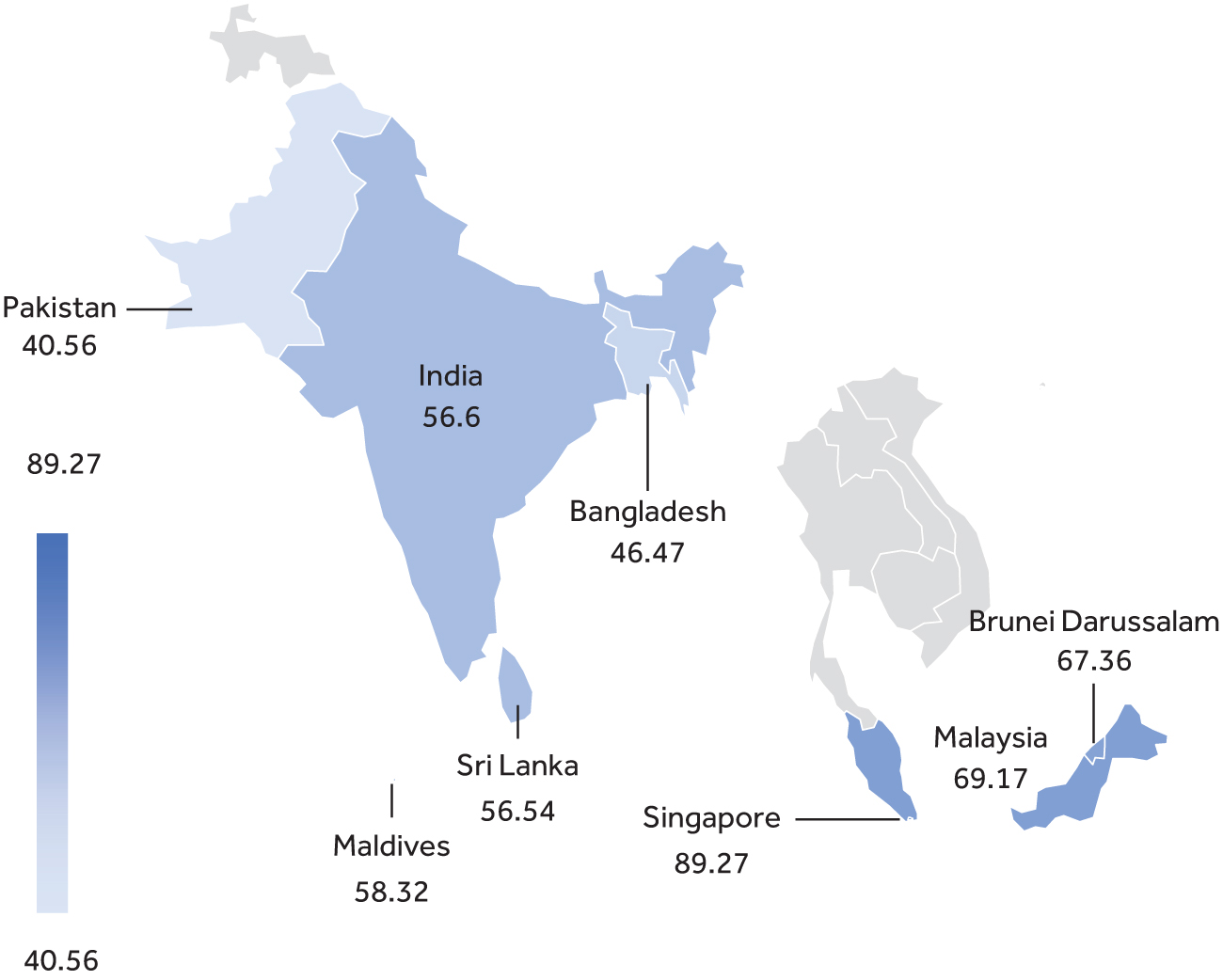

Private sector credit to agriculture remains considerably low in the region. In five of the eight Commonwealth countries in the region for which data is available, allocation of private sector credit to agriculture is highest in India (11.92 per cent).

Table 3.1: Private sector credit to agriculture

|

India |

11.92% |

|

Sri Lanka |

7.48% |

|

Malaysia |

1.91% |

|

Singapore |

0.33% |

|

Maldives |

0.01% |

Particularly, smallholders find it hard to access credit from formal sources because they are not as organised. This is due to the fact that formal financing sources prefer to lend to institutions and organisations that have structures in place.

Smallholders in Asia access financing from other actors in the value chain through informal channels. These actors include input and output distributors. The input chain works in the following ways:

- Agro input manufacturers sell to input distributors, mostly on a cash basis.

- Input distributors provide financing required by smallholders. They do this to lock farmers in and maintain a steady farmer base of customers.

- Credit repayments are made by smallholders upon harvest and sale of produce.

The output chain works in the following ways:

- Output dealers come in the form of small local aggregators who buy produce from farmers.

- They are motivated to lend to smallholders so that they can have an avenue through which they source produce.

- Credit repayments are made by smallholders upon harvest and sale of produce.

Input and output dealers do not require collateral from the smallholders to which they lend. Rather, there is a social understanding, as smallholders and lenders are usually from within the same social setting. The social systems are based on social contracts that typically work. There is evidence that successful credit companies use the concept of social lending to lend to smallholders through farmer producer organisations that have a network of farmers. In this social lending model, the credit company will lend to the producer organisation that then lends to its members. This model works because members feel liable to the producer organisation or a farmer collective.

3.2.3 Market, trade and supply chain

Logistical challenges. The output produced by smallholders is typically too small to fill up a truck that is the preferred mode of transportation of commodities to market. It is therefore not always viable to transport produce to market because, given what is spent on transport, they would have to be a minimum price/volume that would have to be guaranteed. The resultant factor is smallholders are now reliant on local aggregators who typically bulk for multiple farmers in the community and then transport it to the market.

Information asymmetry. Smallholders do not always know the right markets to sell to, the prices at which to sell, and the best way to access markets. Market information and access is easier for aggregators and bigger farms since they are aware of the product off-takers, their needs and their prices.

Leveraging agri-commodity markets provides an avenue for farmers, producers and other actors in the value chain to gain access to indicators on prices for agricultural products which is bound to reduce price volatility. For example, in India, there are six national-level commodity exchanges; some of which offer electronic spot exchanges which allows for spot trading of agri-commodities. ITC-ABD, one of the largest aggregators and exporters of Indian agri-commodities, utilises the commodity markets to hedge the price risk. Participation of a majority of farmers in such commodity markets is, however, still low which points to a need for increased sensitisation on its benefits.

3.2.4 Gender mainstreaming

Table 3.2: Employment in agriculture

|

Employment in agriculture, female (% of female employment) |

|

|

Commonwealth Asia Average |

26.71 |

|

Bangladesh |

57.57 |

|

Brunei Darussalam |

0.72 |

|

India |

54.69 |

|

Malaysia |

5.89 |

|

Maldives |

2.00 |

|

Pakistan |

65.18 |

|

Singapore |

0.01 |

|

Sri Lanka |

27.63 |

Source: World Bank Data.[9]

Source: FAO.[10]

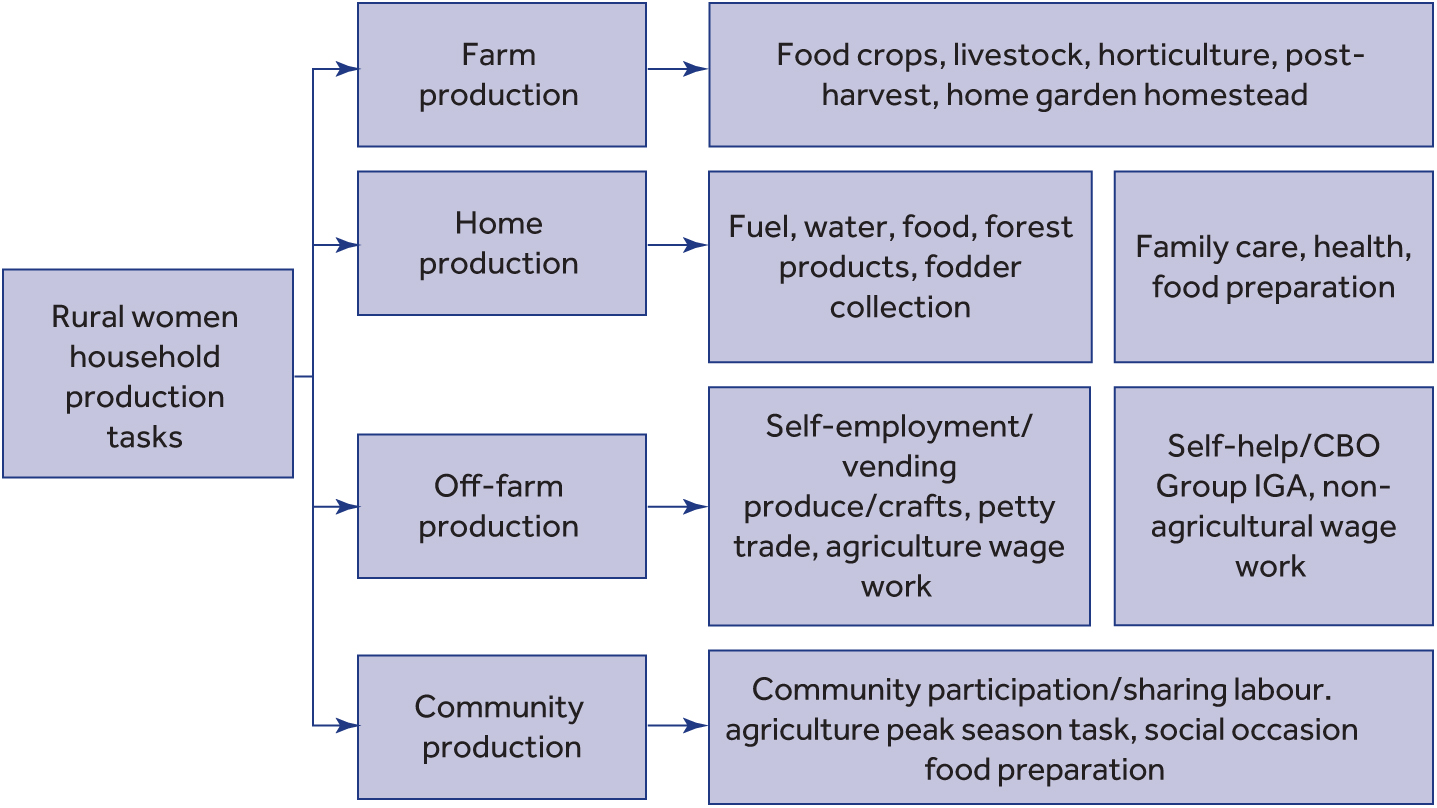

The agriculture sector employs a high proportion of the women in South-Asian Commonwealth countries (Bangladesh, India, Pakistan and Sri Lanka). Except for Sri Lanka, the agriculture sector employs more than half of the women in Commonwealth South-Asia. The ways in which women in Commonwealth South-Asia participate in agriculture is shown below.

Noteworthy is the fact that rural women engage in more than just the above activities. In Commonwealth South-East Asia (Brunei Darussalam, Malaysia and Singapore), the agriculture sector is not very significant when it comes to women employment. In Malaysia, women are highly engaged in the fish value chain, which is out of the scope of this study. The challenges that are faced by rural Asian women (such as low levels of literacy, limited access to finance and agriculture land) are similar to those faced by rural African women.

3.2.5 Youth employment and entrepreneurship

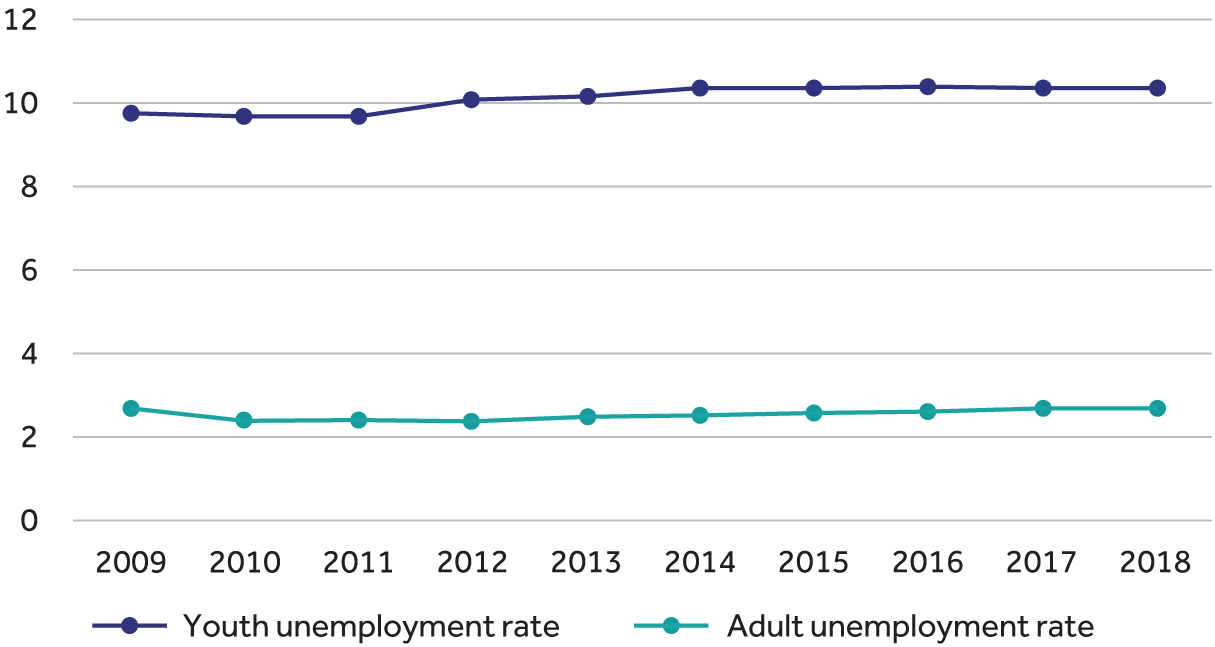

In South-Asian Commonwealth, the youth unemployment rate is and has historically been higher than the adult unemployment rate. Noteworthy is the fact that although unemployment rates are generally low, most of the employment that is available to the youth is informal.

Source: ILO.[11]

|

Constraints faced by youth participating in agriculture |

|

Compared to adults, the youth in agriculture have less access to land and financing. |

|

Lack of access to land is a key factor behind the unemployment of youth in farming communities.[12] |

|

Regarding access to land, inheritance norms mean that young people have to wait for a considerable amount of time before they can inherit the land which includes agricultural land. When it comes to the inheritance of agricultural land, female youth are disadvantaged as cultural norms dictate that the land is inherited by male heirs. This trait is consistent with the current situation in Africa. Additionally, dividing up land among the male children in families has led to increased land fragmentation and reduced farm sizes. |

|

Regarding access to financing, land titles are typically the preferred form of collateral, and as previously mentioned, the youth have limited access to agricultural land. Additionally, other forms of collateral such as the existence of formal occupation, immovable assets (e.g. land and building), movable assets (e.g. machinery, furniture, equipment), solidarity group guarantees or personal guarantors are not always held by the youth. |

Case study: Impact of the COVID-19 pandemic on the agriculture sector in Commonwealth Asia

Impact of the COVID-19 pandemic

- Labour shortages: In countries like India, 82 per cent[13] of farmers are small and marginal in their operations. Lockdown restrictions halted the movement of prospective labour from village to village resulting in a shortage of harvest labour.[14]

- Disruption in supply channels: Lockdown restrictions coinciding with harvest seasons left farmers unable to transport their produce to markets. This mainly hit perishables such as fruits and vegetables, meat and fish, which are characterised by lower shelf lives than other commodities. For example, on the second day of the initial 21-day lockdown, truck drivers in India abandoned trucks full of agricultural produce on interstate highways citing prolonged traffic queues on the highways. This led to a shortage of agricultural supply among wholesalers in the country.[15]

- Volatility of food prices: Partial or full closure of food markets resulted in shortages of agricultural food supply. This coupled with disruptions in supply channels led to fluctuations in food prices.

- Difficulty in timely marketing and sale of agricultural produce:[16] Lockdown restrictions and closure of physical marketplaces of agricultural produce limited avenues available to farmers to market and sell their produce. This was worsened by the limited digitalisation of agriculture in the region which meant that majority of the farmers could not take advantage of e-commerce platforms to market agricultural produce.

Responses in light of COVID-19 Outbreak

- Leveraging existing digital channels to purchase agricultural produce: To counter difficulties in the sale of post-harvest produce, some private entities utilised existing digital infrastructure to purchase produce from farmers.

- Stimulus packages: Following the start of the pandemic, most governments issued financial packages to protect vulnerable groups including farmers. For example, the Indian Government’s finance ministry issued a 1.7 trillion Indian rupees package following the initial lockdown to cushion the impact of the pandemic.

- Easing the burden of debt financing on agro-loans: Farmers and agribusinesses with existing agricultural loans were granted a grace period by banks to allow for adjustment to prevailing economic climate in the midst of the outbreak.[17]

3.3 State of digital agriculture in Commonwealth Asia

3.3.1 Digital innovations for digitalisation of agriculture in Asia

Digital agricultural solutions and services

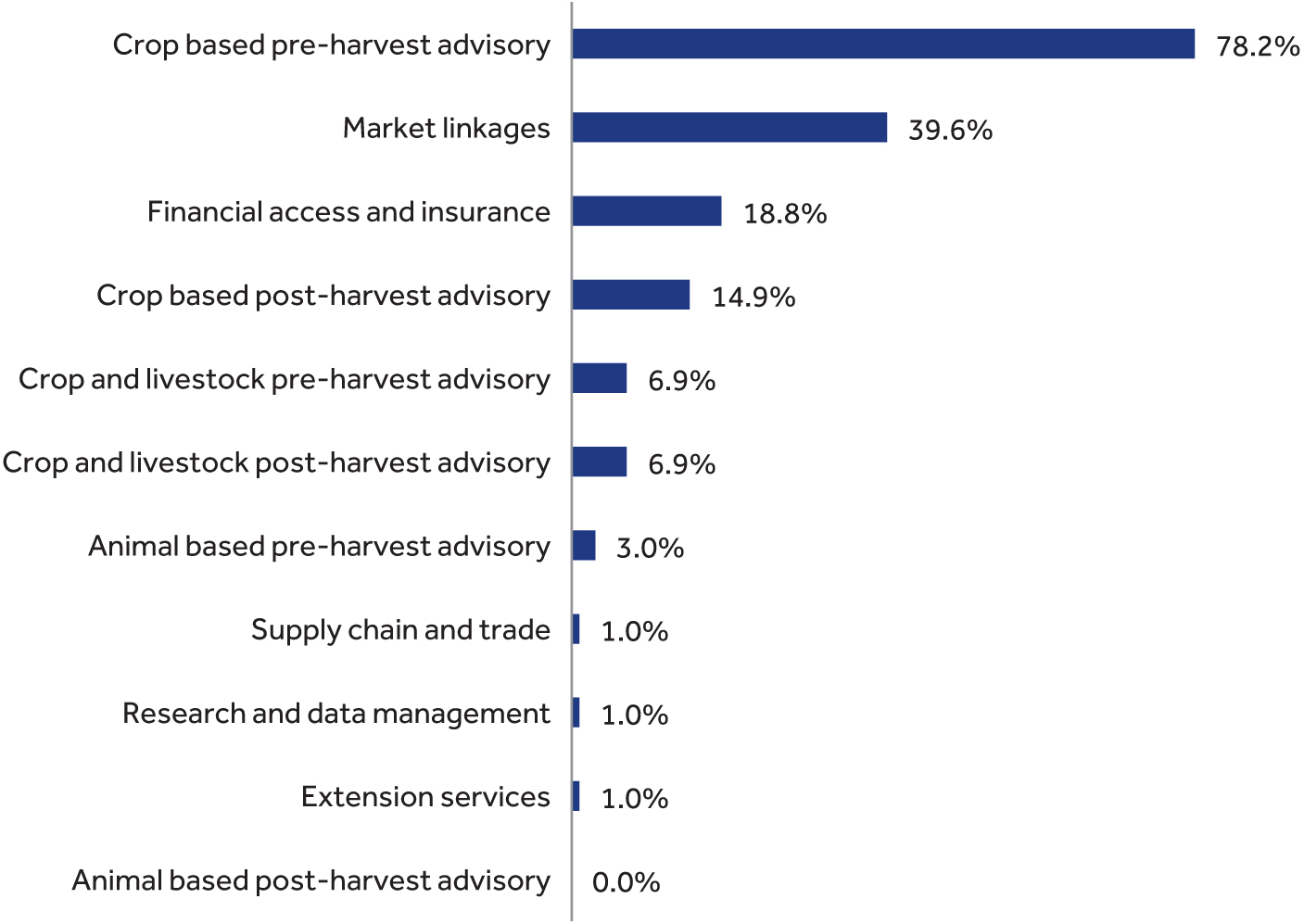

Use cases of digital solutions in Commonwealth Asia

- The assessed solutions were found to be predominantly crop-based pre-harvest advisory solutions (78 per cent).

- The market linkage solutions were also found to be 40 per cent of the assessed solutions.

- Only 19 per cent of the accessed solutions provided a service offering that included financial access and insurance. With less than 12 per cent of all formal private sector lending portfolios going to agriculture[18] in the region, this statistic reveals a significant void in the agricultural financing solutions space.

- While most of the South-Asian region falls far beyond the recommended farmer-to-extension officer ratio,[19] only 1 per cent of assessed solutions provided a means for farmers to access extension agents.

- Eighty-two per cent of the solutions had at most two service offerings, while the remaining 18 per cent had a bundled[20] product offering.

Source: [21]

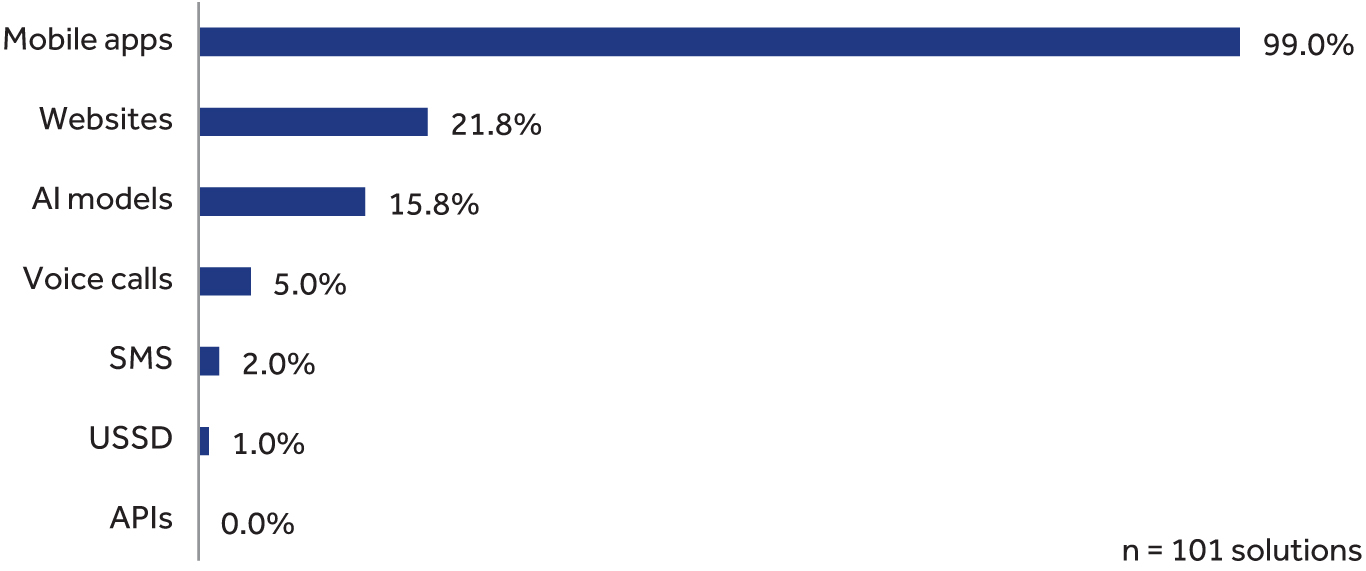

Digital solution delivery means

Most (99 per cent) of the digital agriculture solutions in the sampled Commonwealth Asia are mobile apps. USSD technology is not predominant in the region. The recurrent delivery mediums of the technology used in the region have been elaborated in the chart below.

Characteristics of digital solutions in Commonwealth Asia

1. Crop-based solutions outweigh livestock solutions: Of the assessed 101 solutions, 78 per cent had a crop-based pre-harvest advisory component, while only 3 per cent had an animal-based pre-harvest advisory component

2. Most of the deployed solutions are mobile applications: For the majority (99 per cent) of the assessed solutions, mobile applications were included in their delivery means. Only 1 per cent of assessed solutions used USSD as a primary delivery medium. It is however known that although Asia has the lowest cost of internet in the world, the region has a wide mobile broadband usage gap.[22] This effectively means that more than 90 per cent of developed solutions effectively exclude more than two-thirds of mobile subscribers in the region that use feature phones.[23]

3. The private sector is the main funder of digital solutions: Sixty-six per cent of the solutions are pioneered by private entities, and the remaining 34 per cent were pioneered by state-run entities. The role of the government entities in the development and deployment of digital agricultural solutions may need to be greatly enhanced. Similar to what was observed among African Commonwealth countries, none of the sampled 101 digital agricultural solutions in the region included data from state-run repositories like national farmers’ registries and government provided soil and weather data.

4. Most of the solutions are drawn towards farmer-driven offerings: Except for a few of the applications that link farmers to state-provided extension agents, most of the digital agricultural solutions focused primarily on farmer-driven service offerings.

5. Most of the solutions in Commonwealth Asia have fewer service offerings: Eighty-two per cent of the solutions had at most two service offerings, while the remaining 18 per cent had bundled product offering (two or more service offerings). The finding could also explain the current description of the landscape as a highly fragmented and uncoordinated landscape of solutions with several cases of functionality duplication and consequent inefficiencies. This trend was also recurrent among Commonwealth African digital solutions.

Case study: Featured frontier digital agricultural solution in Asia Krishok Bondhu Phone Seba, Bangladesh

The Government of Bangladesh partnered with UNDP to develop, test and roll out the access to information (www.a2i.gov.bd), the flagship programme. Under the Digital Bangladesh initiative, they developed the Krishok Bondhu Phone Seba, 3331, a hotline that provides an IVR system which farmers can call to receive advisory information from their regional extension agents. When a farmer, who is enlisted with the portal, calls 3331, the call is automatically carried to his/her respective block agriculture extension officer. If the extension officer is unable to pick the call up, the call automatically goes to the supervisor. If the call remains unanswered, the message from the farmer can be recorded and the farmer will receive the answer via SMS. Most IVR helplines for smallholder farmers are dependent on a central call centre, but with this helpline, farmers can reach their area’s block supervisor, thereby reducing the gap between the farmer and agriculture expert.[24]

Value proposition summary

- IVR solution for farmers without internet connections and smartphones.

- Cost-free advisory information from Government extension agents.

- Access to state verified information about agricultural inputs in the region.

- Access to information and insight from university plant researchers.

Product offering details

As with other countries in the region with large numbers of smallholder farmers, dissemination of effective extension services still remains a challenge for national and local governments in the country. In 2018, the government partnered with UNDP to develop a digital solution that would leverage mobile phones, and a web-based portal to bridge the extension gap for smallholder farmers in the region.

In addition, the digital solution is for the first-time enabling extension officers in the country to link national identifier data, farm-level yield data and land identifier data to facilitate the growth of government-provided data-centric digital agricultural solutions in the region. This model of state-led rollout of digital solutions in locations where there are a lot of smallholder farmers is important, especially in the context of other South Asian and African Commonwealth nations. When it is not cost-effective for private entities to build the data infrastructure to be used in digital agriculture solutions, or even for them to roll out digital solutions, government entities can do the initial roll-out and build the requisite data infrastructure in preparation for the future entry of private players in the digital agriculture space in the region.

Smallholder farmer impact

Through the access to Information (a2i-II) Programme, the Krishok Bondhu Phone Seba solution was developed and has gone on to support more than 22 million farming families, by providing them getting extension services from the Department of Agricultural Extension’s 14,000 extension workforce. The digital solution also links extension agents to crop researchers from various universities within Bangladesh. Unlike many digital solutions, this keeps the digital solution with relevant and up-to-date information via constant updates from university researchers.[25]

Farmer impact story: Featured frontier digital agricultural solution Asia (Bangladesh)

The Krishok Bondhu Phone Seba digital agriculture solution features national call service reaching an estimates 21 million farmers for getting agricultural extension services from 14+ thousand extension workforce. When a farmer has a question about his/her farming activities, they dial 3331 to either ask a question directly to extension officers or leave a voicemail if they are unavailable, which will be returned later. If it is a query very specific to the farmer who called, it will be returned via direct person to person call; if it is a query with relevance to the wider group of farmers in an area, then the extension officer records a message, and it is sent to all farmers in the relevant group. If the farmer’s mobile device is already registered with Krishok Bondhu, the call will be directed to a Sub-Assistant Agriculture Officer’s (SAO) mobile number. If SAO is unable to answer, the call will go to his/her line manager, an Assistant Agriculture Officer (AAO). If the AAO is unable to answer, the call will be forwarded to the next level up, the Upazilla Agriculture Officer (UAO). If UAO is unable to answer, then the call will go to voicemail, which will be accessible by the UAO later and action will be taken after analysing the call – Ramesh Chandra Ghosh, agriculture officer

In April 2018, during the Boro paddy season in Mirpur, Kustia picked up his phone and called from “3331-Krishok Bondhu Phone Sheba”. He assumed the sub-assistant and assistant agriculture officer failed to pick up the phone, that is why it was forwarded to his phone. The farmer on the other side began to report his problem. Listening to the farmer carefully, the extension officer understood that the farmers of his area are in danger but still had time to be saved. The Rice Blast disease infection had been observed. He ended the call with advice and prescription to the farmers on the other side. He also informed the farmer of where he could get the required fungicide and the process of applying the fungicide. After the conversation, he called the central officials in charge of 3331 and highlighted the need to take definitive action regarding the situation. He requested to contact 18,000 paddy farmers of Mirpur quickly. The National Agriculture portal has a digital database containing the phone numbers of all these farmers. He sent everyone an urgent SMS message telling them to take immediate action. Krishi Batayan’s team arranged to send the SMS urgently. The next day, Mr. Ramesh the extension office then went out to inspect the field. Going to the field, he was surprised to see that most of the farmers had gone to the paddy field to apply the fungicide after receiving the SMS sent by him. In this way, an agricultural officer was able to save the rice field of 18,000 farmers by using mobile technology.[26]

In summary: how digital solutions are being leveraged to solve systemic constraints

Snapshot on how digitalisation is being used to tackle climate change and enhance agricultural productivity

Climate variability: As with many smallholder farmers, Asian farmers mainly have rain-fed agricultural operations. With farming systems built entirely on the timely arrival of the annual monsoon, the effects of climate change have made its arrival unpredictable and have had consequences reaching far and wide for farmers. Digital solutions are dealing with this challenge by offering weather prediction mobile applications providing localised weather forecasts like in India[27] and applications providing remote access to crop advisory services like in Pakistan.[28]

Agricultural productivity: In this space, current digital solutions provide farmers with access to high-quality inputs, for example, the Pusa Krishi a mobile application in India, and the Kisan Zar Zameen[29] application in Pakistan that provides farmers with access to rentable smart farming technology like drones.

Snapshot on how digitalisation is being used to facilitate youth employment and entrepreneurship

Although agriculture accounts for up to 40 per centof the employed labour in the region, none of the assessed solutions made provisions for youth and youth entrepreneurs.

Use of index-based insurance in Asian Countries in the Commonwealth

As with African Commonwealth countries, South-Asian Commonwealth countries have larger concentrations of smallholder farming populations. Notable insurance schemes in the region have been run by partnerships between Governments and international bodies like the World Bank. A key example is the Government of India's partnership with the World Bank on the National Agriculture Insurance Scheme. Under this partnership, more than 25 million farmers are insured as early as 2010.[30] Despite a large number of insured farmers in the region, lengthy payment periods for claims have affected the effectiveness of agricultural insurance programmes.

Snapshot on how digitalisation is being used to solve market, trade and supply constraints

With many farmers in the region reliant on third-party transport service providers to move their produce to local markets, solutions in the space enable farmers to book spaces on transporter trucks. Examples in this space include the Kisan Rath[31] mobile application in India. In addition, some solutions in the space also link smallholder farmers directly to the final consumers of the produce such as the Govipola[32] application and websites in Pakistan.

Digital technologies use cases in Asian Commonwealth countries

The use of smart farming technologies in Commonwealth Asia, just like in Sub-Saharan Africa, is not well documented. This section highlights some notable use cases of smart farming methods in Commonwealth Asian countries.

1. Optical sensors applied to reduce nitrogen inputs in northwest India. In India, the Agritech company Trimble’s GreenSeeker optical sensing system is being applied to help smallholder farmers to minimise the use of chemical inputs in their farming activities. The GreenSeeker is a solution that computes the normalised difference vegetation index (NVDI) value for individual plants and relays the appropriate information to a network of sensors that apply nitrogen-rich fertilisers according to individual plants.

2. Laser land levelling in southeast Pakistan and northwest India.[33] In India, the Governments of Gujarat and several other regions have subsidised the use of laser-based land levelling technology for smallholder farmers. The region that has been noted to use the technology comprises the states of Sindh and Punjab in Pakistan and Punjab, Rajasthan, Haryana and Gujarat in India. These regions similarly tend to have the highest acceptance rate of smart farming technologies in Southern Asia. Geographically, they represent about 60 per cent of the arable land in Pakistan and 20 per cent in India. Cereal crops are grown commercially and contribute a major portion of procured grain in both countries. The costs and benefits of laser land levelling are relatively even between the two countries aside from roughly 20 per cent higher agricultural input costs and 20 per cent lower labour costs in Pakistan.

3. Crop image diagnosis with the Plantix app. In India and Pakistan, mobile applications like the Plantix app are used for crop disease diagnosis on their mobile phones. Farmers take pictures of the affected crops and upload them using the app. The photographs are analysed using artificial intelligence algorithms, and results are returned immediately to the individual farmer. Critical information on symptoms, triggers, chemicals as well as biological treatments is provided.[34] All pictures sent via the app are geo-tagged, thereby enabling real-time monitoring of pest and disease outbreaks. The resulting metadata provide valuable insights into the spatial distribution of cultivated crops and most significant plant diseases, e.g. in the form of high-resolution maps. Currently, the app has a plant image database of half a million pictures covering 30 crops worldwide and offers prescriptions for over 120 crop diseases.

4. Soil variability assessment. Precision Development, a global non-profit organisation that harnesses technology, data science, and research to empower people living in poverty and improve their lives, is supporting the Government of Punjab, Pakistan on a multi-year endeavour with the goal to make customised mobile-based advisory services to facilitate the effective use of soil health cards. The initial work revolves around complementing the planned distribution of soil health cards with mobile phone-based explanations and encouragement to use the prescribed fertiliser types and amounts. In addition, the firm also offers a more targeted digital solution that assesses soil field variability.

3.3.2 Data infrastructure for digitalisation of agriculture in Asia

Data for content

Soil property data: Four (4) of the eight (8) countries in Commonwealth Asia (Bangladesh, India, Pakistan and Sri Lanka) have state-provided soil health card initiatives. The soil health card is important because it provides information on the properties of the soil. This information can be used by farmers to optimally source and apply nutrients like fertilisers. The extent of penetration of soil card initiatives and utilisation by the target smallholder farmers is not widely documented. Soil moisture and ocean salinity from the European Space Agency[35] also covers all the countries in the region, providing Soil Moisture product data generated respectively within three and four hours from sensing every 48 hours at no cost. Despite this, none of the assessed solutions in the region make use of this open-source data set. Utilising these data could vastly improve the availability of accurate soil property provision.

Weather data: All the Commonwealth countries in Asia have weather data and forecasts provided by state meteorological bodies. However, except for Singapore and Malaysia, Commonwealth countries in Asia countries have no government-issued web Application Programming Interfaces (APIs) for weather data. Lack of state-issued APIs means that providers cannot tap into weather data collected by the state to offer related solutions. Provision of weather data for agriculture sector is currently being done by private sector actors.[36]

Farm-level yield data: Smallholder farmers in the region hardly capture and maintain records of their farm operations. Without the right training and incentives, many farmers do not see the value in recordkeeping. Additionally, smallholder farmers are reluctant to keep records because records keeping takes time and may require farmers to obtain a new skill altogether. Some of the youth that leave rural areas for education and return ideally play a role in teaching better practices such as record keeping, use of technology and others to their families.

Data on users

User identifiers are a critical first step in the creation of a robust data infrastructure that unites person, land, livestock and crop identifiers.

Primary identifiers for farmers

For all the eight (8) member countries in Commonwealth Asia, state-issued digital identity card systems exist. However, data on roll-out of these digital identifiers for the region remain publicly unavailable.

Some critically successful rollouts of these digital identifier programmes in the region stand out. Two of those are the “Aadhaar” digital identifier issued by the Indian Government since 2009 that has been issued to 85 per cent of India’s 1.2 billion people, and the Pakistan computerised national identity card operated by the National Database and Registration Authority since 2007 that states 96 per cent of its citizens have been issued digital national identifiers. The two bodies also state that this unique identifier has been linked to the national land registries and statutory banking records. While both registries have had numerous challenges with roll-out and ethical concerns, they have had numerous successes in the agritech space.[37] A case in point is the use of the national Aadhaar database by the Indian Government to deliver subsidised fertilisers and the large-scale Public Distribution System (PDS), which provides subsidised food to many rural residents.

User identifiers

Farmer identifiers: With the exception of India and Sri Lanka, no other country in Commonwealth Asia has an active national farmers registry. It should however be noted that variables captured in farmer registries are not available publicly.

Land identifier data: In the rural South Asian Commonwealth, arable land is the most important form of property. Any significant improvement in the farmer economic and social situation is crucially tied to having independent land rights.[38] Across the region, land ownership is broadly determined by access to a land certification document that states such ownership or user rights. Data on the state of formal registration of land remain largely inconclusive.

For most of the smallholder farmers in the region, land is mainly informally administered, and where formal administration procedures exist, there is a wide variation in the certification process, and the properties of the resultant document.

In many of the countries in Commonwealth Asia, land ownership is determined through various records such as registered sale deeds, property tax documents, and Government survey records. Small and marginal farmers, who account for more than half of the total land holdings, often do not hold formal land titles, and administer the land in their possession informally.[39]

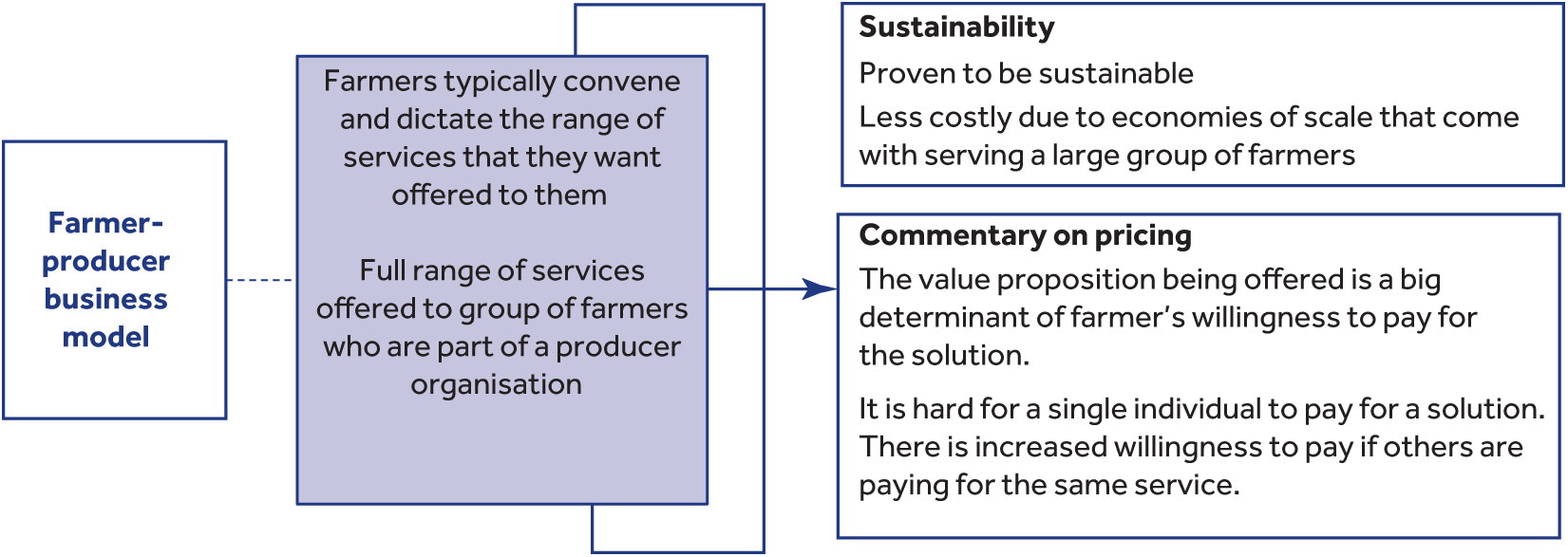

3.3.3 Business development services for digitalisation of agriculture in Asia

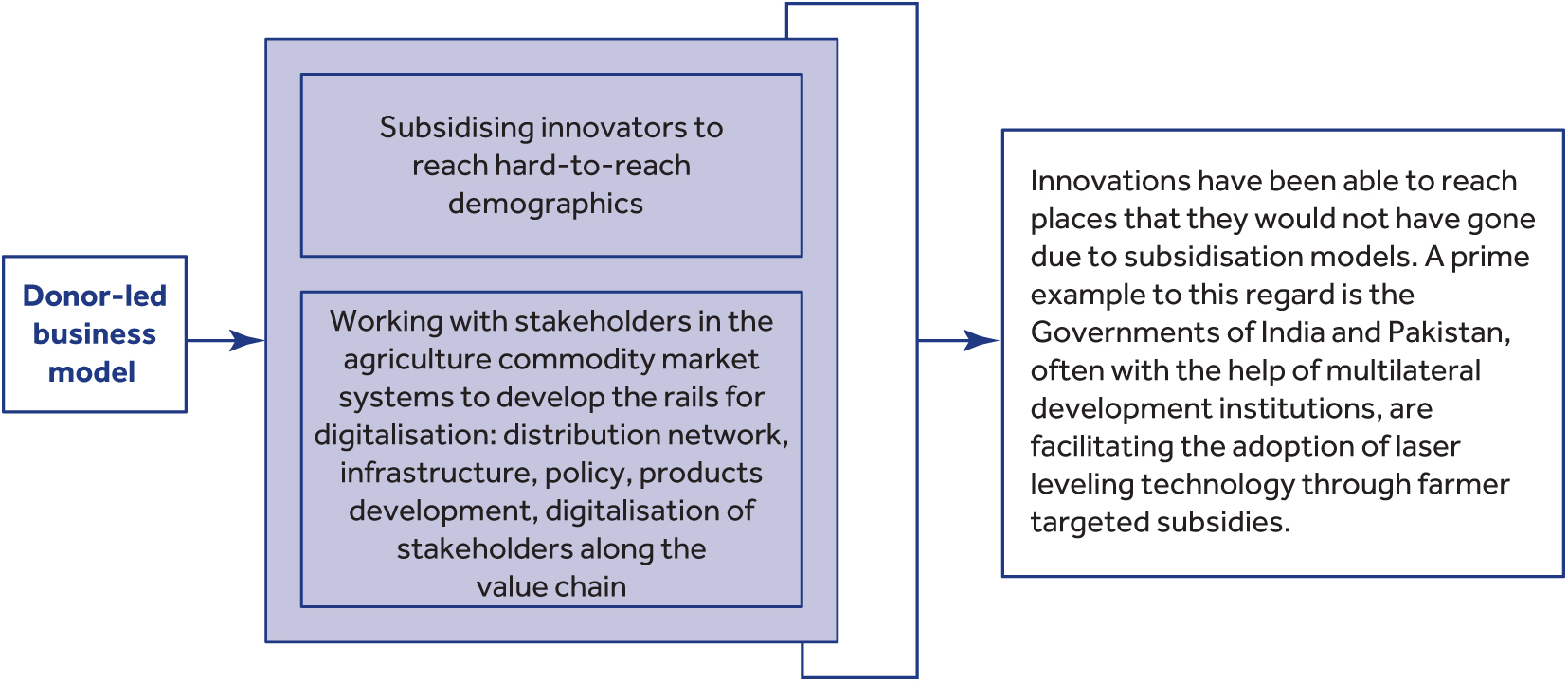

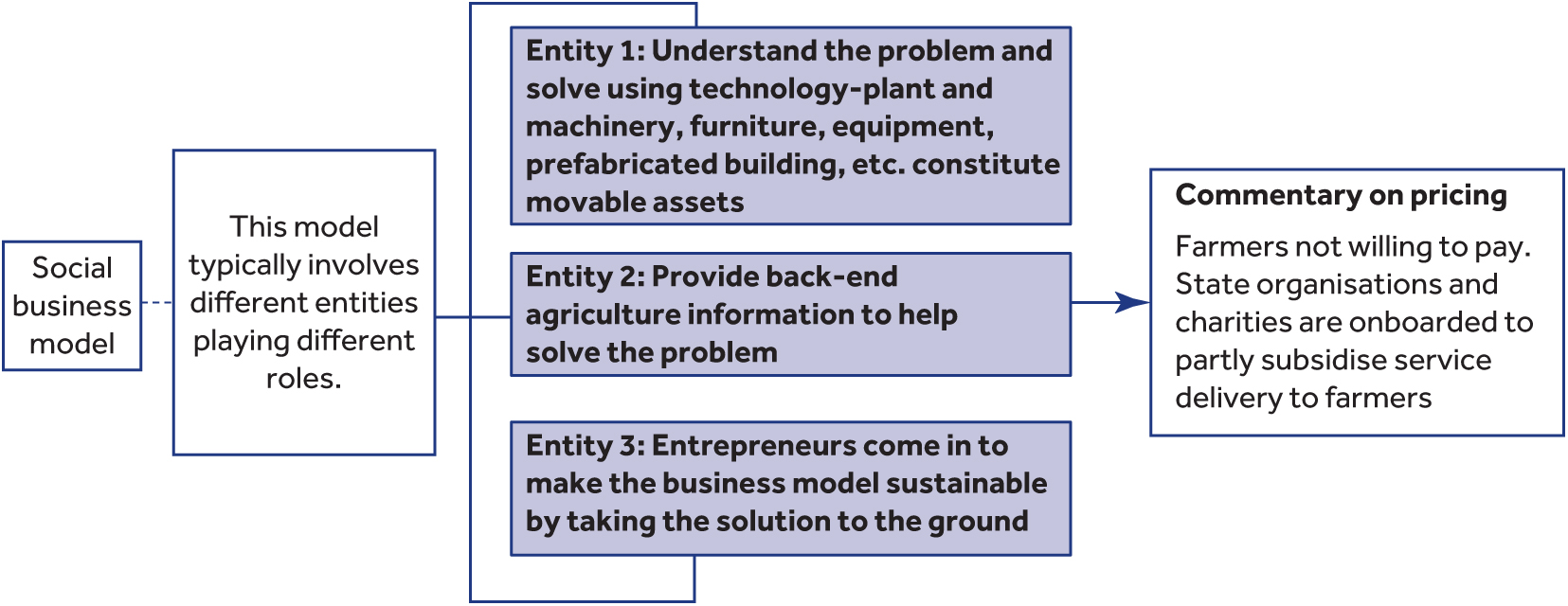

Key business models

For the case of Asia, four models have been illustrated below.

3.3.4 Enabling environment for digitalisation of agriculture in Asia

Technology-related enablers of digital adoption

1. Adoption of mobile devices: Mobile devices are what is the primary access medium to the internet. This makes access to mobile devices a big driver for the adoption of digital agriculture solutions. The last couple of years have seen an increase in mobile phone penetration in Asia. In the next 5 years, the proportions of mobile service users are expected to increase by up to 6 per cent in South Asia.[41] Mobile cellular subscriptions for Commonwealth Asia are shown below.

Table 3.3: Mobile cellular subscriptions (per 100 people)

|

Mobile cellular subscriptions (per 100 people) |

|

|

Bangladesh |

102 |

|

Brunei Darussalam |

132 |

|

India |

84 |

|

Malaysia |

140 |

|

Pakistan |

76 |

|

Singapore |

156 |

|

Sri Lanka |

144 |

Source: World Bank Data.[42]

2. Availability of network coverage and internet access: The proportion of the population that uses the internet in Commonwealth Asia varies from the lows of 13 per cent in Bangladesh and 17 per cent in Pakistan to the highs of 89 per cent in Singapore and 95 per cent in Brunei Darussalam.

Table 3.4: Individuals using the internet (% of population)

|

Individuals using the internet (% of population) |

|

|

Average |

52.00 |

|

Bangladesh |

12.90 |

|

Brunei Darussalam |

95.00 |

|

India |

34.40 |

|

Malaysia |

84.21 |

|

Pakistan |

17.07 |

|

Singapore |

88.95 |

|

Sri Lanka |

34.11 |

Source: World Bank Data.[43]

Non-technology related enablers for digitalisation

1. Young population demographics: In Asia, the proportion of people aged below 40 is 62.5 per cent, rising as high as 65.4 and 70.2 per cent in South and Southeast Asia (where the eight Asian Commonwealth states are located). This youthful demographic born after the 1990s is more familiar with the internet and is estimated to have a much higher acceptance of internet-related advances as well as a much faster learning curve in working with digital agricultural solutions.

2. Targeted Government subsidies: The kind of farming support that is available (irrigation-based, linkages to market, support from extension support) plays a part in the adoption of technology. A case in point is the state Government of (Odisha) India support of the Ama Krushi crop advisory solution.[44] Support from the state and regional Governments in these regions reduces the cost of deployment of digital agriculture solutions especially in the cases where state Governments provide financing and crop production extension officers.

Non-technology-related barriers to digitalisation

1. Low farmer literacy: As is the case in Africa, low farmer digital literacy significantly affects their ability to adopt and use digital solutions. A case in point is the interaction of farmers in India with the Government issued soil health cards. Although more than 100 million soil health cards had been issued to farmers by 2018, researchers with the Cereal Systems Initiative for South Asia revealed significant usage difficulties by farmers as they did not understand the printed information.[45]

In conclusion, the technical, and regulatory environments regarding digitalisation of agriculture in the region vary across countries with some countries being better off than others (based on the GSMA[46] mobile Connectivity Indices for Commonwealth Asia countries). Like the African Commonwealth countries, mobile devices in this region play a significant role in the consumption of digital agricultural solutions.[47] This section uses the GSMA Mobile connectivity index as a quantitative description of the state of digitalisation of agriculture. This is because the GSMA Mobile Connectivity Index measures the enablers of mobile internet connectivity. With the exception of South-East Asian Commonwealth member countries like Singapore, Malaysia and Brunei with connectivity indices higher than 60, all South-Asian Commonwealth countries still have national connectivity indices greater than 60.

This index has been explained in detail in both the annex and footnote below

The GSMA Mobile Connectivity Index[49] measures the enablers of mobile internet connectivity. This index provides an aggregated quantifiable measure for selected indicators enablers of mobile connectivity. These indicators are as follows: Infrastructure – the availability of high-performance mobile internet network coverage; Affordability – the availability of mobile services and devices at price points that reflect the level of income across a national population; Consumer readiness – citizens with the awareness and skills needed to value and use the internet, and a cultural environment that promotes gender equality; Content – the availability of online content and services accessible and relevant to the local population.

3.4 Policy recommendations to fast-track digitalisation of agriculture in Asia

3.4.1 Digital innovations

Gaps (factors limiting innovation and scalability in digital agriculture)

- Lower usage and adoption of digital solutions among women.

- Low mobile penetration in rural areas.

- Significant number of solutions are still reliant on broadband connectivity to deliver their value propositions. As with the solutions in African Commonwealth Countries, many digital agriculture solutions are built with mobile applications, sensors and websites as their primary delivery mediums. This means that many of the current digital agriculture solutions are inaccessible without mobile broadband connections.

Table 3.5: Recommendation for Asian countries to increase investment in digital agriculture innovations

|

A. Use support measures to increase usage of digital solutions |

Real-world examples where the suggested measures have been used |

|

|

A.1 Reduce the import tariffs on mobile devices and tax rates on mobile broadband connections. |

Argentina – In Argentina, a study by the GSMA estimated that the elimination of excise duty on mobile services would generate an increase in tax income of about $980 Million per year, in only 4 years. It would also bring 1.7 million additional people online, significantly reducing the digital divide, and increasing internet usage for those that were already users. This can hence be used as the basis for the argument against internet-related taxes since the multiplier benefits from the usage of mobile devices far out weights the tax revenue[50] |

|

|

B. Formulate strategies that enable all people to participate and excel in the digital economy |

Real-world examples where the suggested measures have been used |

|

|

B.1 Leverage the power of societal “gatekeepers” |

India – The use of internet “Saathis” has been used with considerable success in some parts of rural India to help people in rural areas acquire the required digital literacy to enable them to use the internet effectively. In addition, “Saathis” have helped bridge the gender divide in the use of internet and mobile devices to consume digital services. Launched by Google India and the Tata Trusts Collectives for Integrated Livelihood Initiatives, Google’s Internet “Saathis” addresses the digital gender gap in India by facilitating digital literacy among rural women. The Programme trains women to become master trainers, or “Saathis”(companions), who are given a smartphone or tablet and a bicycle to help women in their villages experience the benefits of the internet[51] |

3.4.2 Data infrastructure

Gaps in the data infrastructure required for digitalisation of agriculture to thrive

- Absence of state-run soil and weather data APIs. Except for Sri Lanka, none of the other states in the region have Government-provided weather Application Programming Interfaces (APIs) to facilitate the use of state-provided weather data in private sector digital agriculture solutions.

- Absence of interoperability and robust linkages between land and person identifiers. While all the governments in the region have nationwide campaigns to distribute national identifiers, definitive links between land, person and livestock identifiers remain largely non-existent.

- Significant percentage of land under customary tenure. Despite deliberate formalisation attempts by the governments in the region, a large amount of the land held by farmers in the South Asian Commonwealth is still informally administered.

Table 3.6: Recommendation for Asian Countries to increase investment in data infrastructure

|

C. Boost investment in digital data infrastructure and their key enablers |

Real-world examples where the suggested measures have been used |

|

C.1 Investing in regular decennial agricultural census activities |

Kenya – Every ten years, as advised by the Food and Agriculture Organisation of the United Nations (FAO). The Kenya Bureau of statistics executes a decennial agriculture Census and publicly avails the resultant data sets. This enables the digital solution developers to customise their digital agriculture solutions such that they are in line with the demands of the farming population as revealed in the survey data[53] |

|

C.2 Package Government issued weather data as open APIs Governments could package soil and weather data in form of open APIs1 such that solution developers can easily include these data in their solutions at no cost, rather than undertaking expensive processes to collect it on their own. Creating and opening up APIs would reduce the cost of acquiring data for solution developers. This would trickle down into reduced cost for the end user |

South Africa – In South Africa, the Government mandated metrological entity invests in the distribution of both historical data and the anticipated weather forecast data via an Open API. This provides a direct opportunity for digital solution to include state-collected data in their solutions at no cost |

|

C.3 Inclusion of freely available high-quality data solutions in developed digital solutions Large amounts of freely available data from entities such as the European Soil Moisture and Ocean Salinity (SMOS) data project are existent and highly relevant. Governments could leverage these data and make it accessible to actors in the value chain through APIs |

Canada – The Canadian Government invested in the web and mobile applications to distribute Soil Moisture and Ocean Salinity (SMOS) data from the European Space Agency. These data is availed in addition to that provided by private soil testing entities. This data can also be accessed and provided to digital solution developers in Asian Commonwealth Countries[54] |

|

D. Develop national strategies for issuing identifiers and improve interoperability among frameworks |

Real-world examples where the suggested measures have been used |

|

D.1 Issue of identifiers India has had considerable success in rolling out its state identifier system. While this is not yet linked to farm level and land identifiers, it is a welcome first step in the right direction. Other Commonwealth countries in Asia could also enhance efforts to roll out unique person identifiers, which they can later link to farm level and land data sets, in order to foster the creation of relevant data-driven digital agricultural solutions |

India – The Indian Government has succeeded in distributing the national 12-digit identifier the Aadhar to more than 1.2 billion people, including an estimated 120 million farmers[55] |

|

D.2 Improve interoperability among systems and frameworks Where different identifiers have been issued, it is recommended that system linkages are made so that the systems can speak to each other. Person identifiers should be linked to land, crop and livestock identifiers to enable policy-makers to have a concrete basis to make data-driven decisions |

Uganda – The German foreign ministry through GIZ partnered with the Ugandan Ministry of lands, housing and urban development to issue land certificates to smallholder farmers in the Eastern Ugandan districts of Soroti and Katakwi. The initiative used state-issued national identifiers and linked these to a digital land registry to be used to document the land use rights of collectively held agricultural land[56] |

3.4.3 Business development services

Gaps (factors hindering the flow of financing to digital innovations in agriculture)

- There are many smallholders. Most of whom do not understand the case for digitalisation. Despite Government efforts, the South-Asian region still has the largest number (more than 100 million) of family and smallholder food producers in the world. These farmers, fishers and herders produce more than 80 per cent of the food consumed in the region. Smallholder farmers are usually subsistent producers, which reduces their incentive to consume digital agriculture solutions. The problem is exacerbated by the fact that most smallholders lack digital literacy skills and earn low margins.

- Low state provided expenditure on Government research and development into smart farming. An increasing number of countries are experiencing a steady rise in agricultural R&D spending since 2000. But in South Asia, Government expenditure in agriculture has declined or has been very low in all countries except in India. In Bangladesh, Pakistan and Sri Lanka, agricultural growth has slackened during the same period. This means that the region is primarily reliant on digital research and development funding from the private sector.

Table 3.7: Recommendation for Asian countries to increase investment business development

|

E. Use farmer groups as a gateway for extending digital agriculture solutions to smallholders |

Real-world examples where the suggested measures have been used |

|

E.1 Identify cooperatives and use them as a pathway for conducting capacity building of smallholders. |

Uganda – The Ugandan Agritech startup Ensibuuko develops digital solutions to provide last mile financing options for smallholder farer groups. In addition, the startup provides crop insurance to farmer groups in Southwestern Uganda. Digital solution developers in the Commonwealth Asian nations can be given incentives by Governments to ensure solutions are developed directly for farmer groups not individual smallholder farmers as solutions developed to target groups of farmers have a higher adoption rate than those developed for individual farmers |

3.4.4 Enabling environment

Gaps in the enabling environment required for digitalisation of agriculture to thrive

- Limited knowledge on the use of mobile broadband – The GSMA estimates that more than 40 per cent of Indian adults were not aware of mobile internet, compared to over 30 per cent in Pakistan and Bangladesh by 2019. This leaves a significant number of potential digital agriculture solution consumers excluded from the consumption pool.[57]

- Significantly high level of illiteracy and digital illiteracy – UNESCO estimates that South Asia alone is home to almost half of the global illiterate population (49 per cent). This means a large proportion of the people can understand and utilise digital agriculture solutions.[58]

- Prohibitive fiscal environment – Some Asian Governments apply a number of different and often special taxes to the mobile network providers over and above the general taxation applied to other sectors of the economy, despite the positive externalities of mobile goods and services. This has a consequence of making the cost of broadband connections prohibitively high.

Table 3.8: Recommendation for Asian countries to create an enabling environment for digitalisation to thrive

|

F. Securing digital inclusiveness |

Real-world examples where the suggested measures have been used |

Pillar/element that the suggested recommendation responds to |

|

F.1 Engaging with actors in the ecosystem to incorporate deliberate inclusive initiatives in their design |

Rwanda – In 2014, the Rwandan Ministry of Education signed an agreement in partnership with Microsoft. The agreement enabled the use of new digital technologies and the acquisition of new competencies in the new technologies domain to transform the national educational field. The Rwandan Government’s “Smart Classrooms Initiative” programme, aiming at furnishing more than a thousand classes with an Internet connection, is one of the components of this agreement. The initiative effectively enables students to experience the internet and acquire the required digital skills that will be critical in enabling them to consume digital solutions in the future with minimal hardship[59] |

Data Innovations |

|

F. Securing digital inclusiveness |

Real-world examples where the suggested measures have been used |

Pillar/element that the suggested recommendation responds to |

|

F.2 Formulating standards to guide use and implementation of digital technologies and advanced technologies (e.g. Blockchain, satellite imaging, AI and 5G). |

Rwanda – Unlike several other countries in the region, the Rwandan Government has invested heavily in the creation of regulations covering various aspects of recent technology like drones and consumer data protection[60] |

Data Innovations |

|

F.3 Provide targeted subsidies to facilitate digital solution adoption. |

Pakistan – Subsidy programmes initiated by the Governments of India and Pakistan, often with the help of multilateral development institutions, helped facilitate the adoption of laser leveling technology on a greater scale. One of the key advances was the provision of technology-specific subsidies to borrowers for the initial purchase of laser leveling equipment as well as for the interest payments for those that had acquired them on credit[61] |

Business Development Services |

In conclusion, the most undeveloped element of the D4Ag structure in this region is the ‘base’ of an enabling environment pillar in the region is the enabling environment. The South Asian region has made notable progress in accelerating deployments of 4G.[62] In 2020, GSMA estimates that most of the expansion in 4G coverage in the world was in Asia.

However, despite the significant broadband coverage milestones made in the region, several aspects of the enabling environments, specifically, the readiness of the consumers to make use of available digital agriculture solutions remain largely underdeveloped. Lack of awareness is a key barrier to the adoption of mobile internet and the consumption of digital agriculture solutions. Additionally, GSMA estimates that more than 40 per cent of Indian adults were not aware of mobile internet as compared to over 30 per cent in Pakistan and Bangladesh in 2019. For those that are aware of mobile internet, illiteracy and insufficient digital skills persist as the main barrier for more than a third of mobile users in South Asian countries.

The following are necessary for the recommendations to yield results.

- Strong implementation. That is, policies need to be backed by clear strategic and implementation plans: For the policy recommendations and state authored policy tools to have an impact, there is a need for strategic plans that stipulate specific strategic objectives and well-defined activities whose execution would lead to the realisation of the desired impact. In addition, the design of implementation plans should take a multi-stakeholder approach that encourages the involvement of not just the policy-makers, but also regional governments, civil society organisations and most importantly smallholder farmers.

- Capacity building at a policy level is required. Investing in growing the awareness of mobile internet and its benefits, alongside promoting digital knowledge and skills is important to improve access to and adoption of the mobile internet. Mainstreaming digital skills into school curricula or using agent networks to provide training are both ways to improve awareness and skills. Digital skills programmes should aim to strengthen confidence in digital technologies, educate about potential online harms and use locally relevant content that considers the various unique aspects of the end user’s operating domain.

Having an empowered pool of policy and regulation actors would equally have trickle-down effects on policies that are passed.

Digital Agriculture report homepage Next chapter Back to top ⬆

[1] Food and Agriculture Organisation of the United Nations, FAOSTAT. Data retrieved on August 8, 2021. Retrieved from http://www.fao.org/faostat/en/#data

[2] Economic Report (2016). Asia-Pacific: agricultural perspectives. https://economics.rabobank.com/publications/2016/february/asia-pacific-agricultural-perspectives/

[3] Fukagawa, N.K. and L.H. Ziska (2019). Rice: Importance for Global Nutrition.

[4] OECD (2018). Agricultural Policy Monitoring and Evaluation.

[5] CGIAR (2018). Write-up on the state of climate vulnerability in Bangladesh. https://ccafs.cgiar.org/es/regions/sur-de-Asia/Bangladesh

[6] CGIAR (2018). Write-up on the state of climate vulnerability in Pakistan. https://www.adaptation

[7]Pakistan | UNDP Climate Change Adaptation (adaptation-undp.org) (accessed on July 14, 2021).

[8] Chen, C., I. Noble and J. Hellmann (2015). University of Notre Dame Global Adaptation Index. https://gain.nd.edu/our-work/country-index/matrix/

[9] The World Bank, The World Bank Indicator database. Data retrieved on August 8, 2021. Retrieved from https://data.worldbank.org/indicator/SL.EMP.TOTL.SP.ZS

[10] Food and Agriculture (2015). Rural women in household production: Increasing contributions and persisting drudgery. http://www.fao.org/3/af348e/af348e07.htm

[11] International Labour Organization (2014). Global Employment Trends. https://www.ilo.org/wcmsp5/groups/public/---dgreports/---dcomm/---publ/documents/publication/wcms_233953.pdf

[12] International Fund for Agricultural Development (2019). Investing in rural youth in the Asia and the Pacific region. https://www.ifad.org/documents/38714170/41187395/18_Briones_2019+RDR_BACKGROUND+PAPER.pdf/48ab25bb-6a55-e883-bfe3-053348a4b865

[13] The Food and Agriculture Organization (2020) in India. http://www.fao.org/india/fao-in-india/india-at-a-glance/en/

[14] Jadhav, R., Bhardwaj, M. and Thukral, (2020). Coronavirus lockdown leaves no-one to harvest India's crops. https://www.reuters.com/article/health-coronavirus-india-harvests-idINKBN21J4W3

[15] The Times of India (2020). Day 2 of lockdown: Truckers abandon vehicles, delivery boys fret about safety. https://timesofindia.indiatimes.com/india/day-2-of-lockdown-truckers-abandon-vehicles-delivery-boys-fret-about-safety/articleshow/74838109.cms

[16] UNESCAP (2020). Impact of Covid-19 On Agriculture in the Asia-Pacific Region and Role of Mechanization. https://www.unescap.org/news/impact-covid-19-agriculture-asia-pacific-region-and-role-mechanization#

[17] CGIAR (2020) Containing COVID-19 impacts on Indian agriculture. https://www.cgiar.org/news-events/news/containing-covid19-impacts-on-indian-agriculture/

[18] Obtained from author computations from FAOSTAT.

[19] Blum, M. and J. Szonyi (2011). Investment requirements in extension to achieve zero hunger and adapt to climate change.

[20] Food and Agriculture Organization of the United Nations Farming Systems and Poverty. http://www.fao.org/3/y1860e/y1860e07.htm

[21] In this classification, digital agriculture solutions enabling the provision of extension services by linking rural smallholder farmers to extension service providers solution providers are assessed differently from the solutions that provide direct pre-harvest crop advisory for farmers like access to information regarding planting routines, inputs and more.

[22] In our classification, the word bundled was used to refer to digital solutions that has more than two service offerings in their value propositions.

[23] Global System for Mobile Communications, Mobile Internet Connectivity 2020 South Asia Factsheet. https://www.gsma.com/r/wp-content/uploads/2020/09/Mobile-Internet-Connectivity-South-Asia-Fact-Sheet.pdf (accessed on July 10, 2021).

[24] Digital Green (2018). ICT4AG Handbook A quick guide to ICT solutions for smallholder farmers.

[25] Key informant interview with Md. Tanvir Quader (Senior Software Engineer a2i Programme – Bangladesh).

[26] Key informant interview with staff from the a2i Programme – Bangladesh.

[27] Food and Agriculture Organization of the United Nations, 2016, Agricultural Outlook 2016-2025.

[28] https://apps.mgov.gov.in/details;jsessionid=7C82712062816E65D736B88E2A095EFD?appid=1057 (accessed on July 10, 2021).

[29] https://play.google.com/store/apps/details?id=pk.com.pakzarzameen.farmerapp&hl=en&gl=US (accessed on July 10, 2021).

[30] Mahul, O. and N. Verma (2010). Making Insurance Markets Work for Farmers in India. IFC Smart Lessons Brief. World Bank, Washington, DC. © World Bank. https://openknowledge.worldbank.org/handle/10986/10469 License: CC BY-NC-ND 3.0 IGO.

[31] https://play.google.com/store/apps/details?id=com.velocis.app.kishan.vahan&hl=en&gl=US (accessed on 10th July 2021).

[32] https://www.mobileaction.co/app/android/us/govipola/com.fg.krushi (accessed on 10th July 2021).

[33] Whitehead, J. (2014). Developments in Precision Agriculture Use in Asia.

[34] Plantix (2021). Joint Forces Against Highly Invasive Fall Army Worm Pest. https://plantix.net/en/blog/joint-forces-against-highly-invasive-fall-armyworm-pest

[35] Kerr, Y. et al. (2012). ESA's Soil Moisture and Ocean Salinity Mission: Mission Performance and Operations.

[36] These include the open weather map web api (https://openweathermap.org/) and the weather stack api. https://weatherstack.com/ (accessed on July 14, 2021).

[37] Singh, V. and S. Ganguly (2018). Designing a better Soil Health Card for farmers in India. https://www.ifpri.org/blog/designing-better-soil-health-card-farmers-india

[38] Agarwal, B. (1994). ‘Gender and command over property: A critical gap in economic analysis and policy in South Asia’. World Development 22(10).

[39] India Reserve Bank (2015). Report of the Committee on Medium-term Path on Financial Inclusion. https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/FFIRA27F4530706A41A0BC394D01CB4892CC.PDF (accessed on July 10, 2021).

[40] Whitehead, J. (2012). Developments in Precision Agriculture Use in Asia.

[41] Global System for Mobile Communications (2020). The Mobile Economy Asia Pacific 2020.

[42] The World Bank, World Bank indicator database. Data retrieved on August 8, 2021. Retrieved from https://data.worldbank.org/indicator/IT.CEL.SETS.P2

[43] The World Bank, World Bank indicator database. Data retrieved on August 8, 2021. Retrieved from https://data.worldbank.org/indicator/IT.NET.USER.ZS

[44] Precisionag (2020). Frontline delivery in the time of COVID: Ama Krushi in action. https://precisionag.org/frontline-delivery-in-the-time-of-covid-ama-krushi-in-action/

[45] IFPRI (2018). Designing a better Soil Health Card for farmers in India. https://www.ifpri.org/blog/designing-better-soil-health-card-farmers-india

[46] Global System for Mobile Communications, 2020, Mobile Connectivity Index Methodology.

[47] Key informant interview with a technology for development advisor.

[48] The Global System for Mobile Communications, GSMA mobile connectivity index data. Data retrieved on August 8, 2021. Retrieved from https://www.mobileconnectivityindex.com/

[49] The Global System for Mobile Communications index is a quantitative score running from 0 (environment is least enabling) to 100 (environment is most enabling).

[50] Global System for Mobile Communications (2019). Rethinking mobile taxation to improve connectivity.

[51] International Telecommunication Union (2019). Digital skills insights.

[52] https://www.ricult.com/ (accessed on July 10, 2021).

[53] Food and Agriculture Organisation (2020). The future of food and agriculture: Alternative pathways to 2050. http://www.fao.org/3/i6583e/i6583e.pdf

[54] Government of Canada (2021). Satellite SMOS (Sol Moisture Ocean Salinity). https://www.asc-csa.gc.ca/eng/satellites/smos/default.asp

[55] Time (2018). India Has Been Collecting Eye Scans and Fingerprint Records from Every Citizen. Here's What to Know. https://time.com/5409604/india-aadhaar-supreme-court/

[56] Hans-Gerd BECKER (2019). A Fit-for-Purpose Approach to Register Customary Land Rights in Uganda.

[57] Wyrzykowski, R. (2020). Mobile connectivity in South Asia: Huge improvements in mobile broadband coverage bring 640 million online in last five years. https://www.gsma.com/mobilefordevelopment/region/south-asia/mobile-connectivity-in-south-asia-huge-improvements-in-mobile-broadband-coverage-bring-640-million-online-in-last-five-years/#_edn5

[58] UNESCO (2017). Literacy Rates Continue to Rise from One Generation to the Next. http://uis.unesco.org/sites/default/files/documents/fs45-literacy-rates-continue-rise-generation-to-next-en-2017.pdf

[59] Devex (2018). Rwanda could become a model for drone regulation. https://www.devex.com/news/rwanda-could-become-a-model-for-drone-regulation-91868

[60] The East African (2016). Microsoft, Rwanda in deal to promote technology in schools. https://www.theeastafrican.co.ke/tea/rwanda-today/news/microsoft-rwanda-in-deal-to-promote-technology-in-schools-1358752 (accessed on July 10, 2021).

[61] Whitehead, J. (2015). Developments in Precision Agriculture Use in Asia. https://events.development.asia/materials/20120412/developments-precision-agriculture-use-asia

[62] Wyrzykowski, R. (2020). Mobile connectivity in South Asia: Huge improvements in mobile broadband coverage bring 640 million online in last five years. https://www.gsma.com/mobilefordevelopment/region/south-asia/mobile-connectivity-in-south-asia-huge-improvements-in-mobile-broadband-coverage-bring-640-million-online-in-last-five-years/#_edn5

Digital Agriculture report homepage Next chapter Back to top ⬆