Chapter 1: Introduction

1.1 Background to the report

Agriculture ensures food security and employment in most of the Commonwealth member countries. More than half of the population, in 32 of the 54 Commonwealth member countries, reside in rural areas and are engaged in smallholder agriculture. On the other hand, commercial and advanced mechanised methods dominate agricultural production in the developed part of the Commonwealth. As a result, the transformational impact of agriculture-led growth in the Commonwealth cannot be overemphasised. The diversity of the Commonwealth countries – low-, middle- and high-income countries; large or small population size; landlocked, coastal or island countries; and located in Africa, Asia, the Americas, Europe, or the Pacific – uniquely positions it for South–South and triangular cooperation. Despite this diversity, the systemic issues relating to agriculture in the Commonwealth countries remain similar. These include the following:

- Climate variability is especially for the small countries whose export profiles tend to be concentrated in goods and services that are climate sensitive.

- Agricultural productivity is a factor of agriculture-led growth and a ratio of agricultural outputs to inputs that is being impacted negatively by climate variability, reflecting on decreasing agricultural productivity, the basis for trade.

- Market, trade and supply chain is a necessary condition for access to reliable input and output markets – locally and regionally for production and post-harvest management, and a pre-condition for stable income for value chain actors.

- Access to finance and investment, a requirement for market attractiveness, and the emerging role of big data and analytics for alternative credit scoring for financial institutions to manage financial services for agribusinesses.

- Youth employment and entrepreneurship is the foundation for sustaining rural and enterprise development to reduce the rural–urban migration and bridge the gap between the young people seeking work and the available employment opportunities.

- Gender mainstreaming is a key strategy not only for the promotion of equality between men and women, but also for sustainable agricultural and rural development and economic growth as women dominate the lower end of the agricultural value chain.

Despite the above issues, the opportunity is also enormous especially with the power of digitalisation. Digitalisation is seen as a game changer for transforming the agricultural sector.

1.2 Objectives of the report

As countries across the Commonwealth battle with the ongoing COVID-19 pandemic, there is a looming threat of an economic pandemic in the next few years. Understanding the current state of agriculture in the Commonwealth and the role of digitalisation in responding to the health pandemic is required, for medium-term recovery and long-term resilience strategies for economic and sustainable development to be successful. The specific objectives of the report are as follows:

- To review the literature on agriculture in the context of the five regional classifications within the Commonwealth – Africa, Asia, the Americas, Europe and the Pacific taking into consideration the six systemic agricultural issues outlined in the background to the study.

- To review the literature on the three-pillars-and-base of digitalisation for agriculture in the five regions: the state of digital agricultural innovations, the state of agricultural data infrastructure, the state of business development and investment and the state of the enabling environments for digitalisation

- To conduct gap analyses on the current state of play and changes necessary to harness digitalisation within the agricultural sector.

- To produce policy recommendations to leverage the digitalisation of agriculture in enhancing trade and investment in Commonwealth member countries. In making policy recommendations, the report emphasised the pillars that support resilience and make recommendations on the appropriate responses to existent challenges.

1.3 Methodology

1.3.1 Approach used to define digitalisation of agriculture

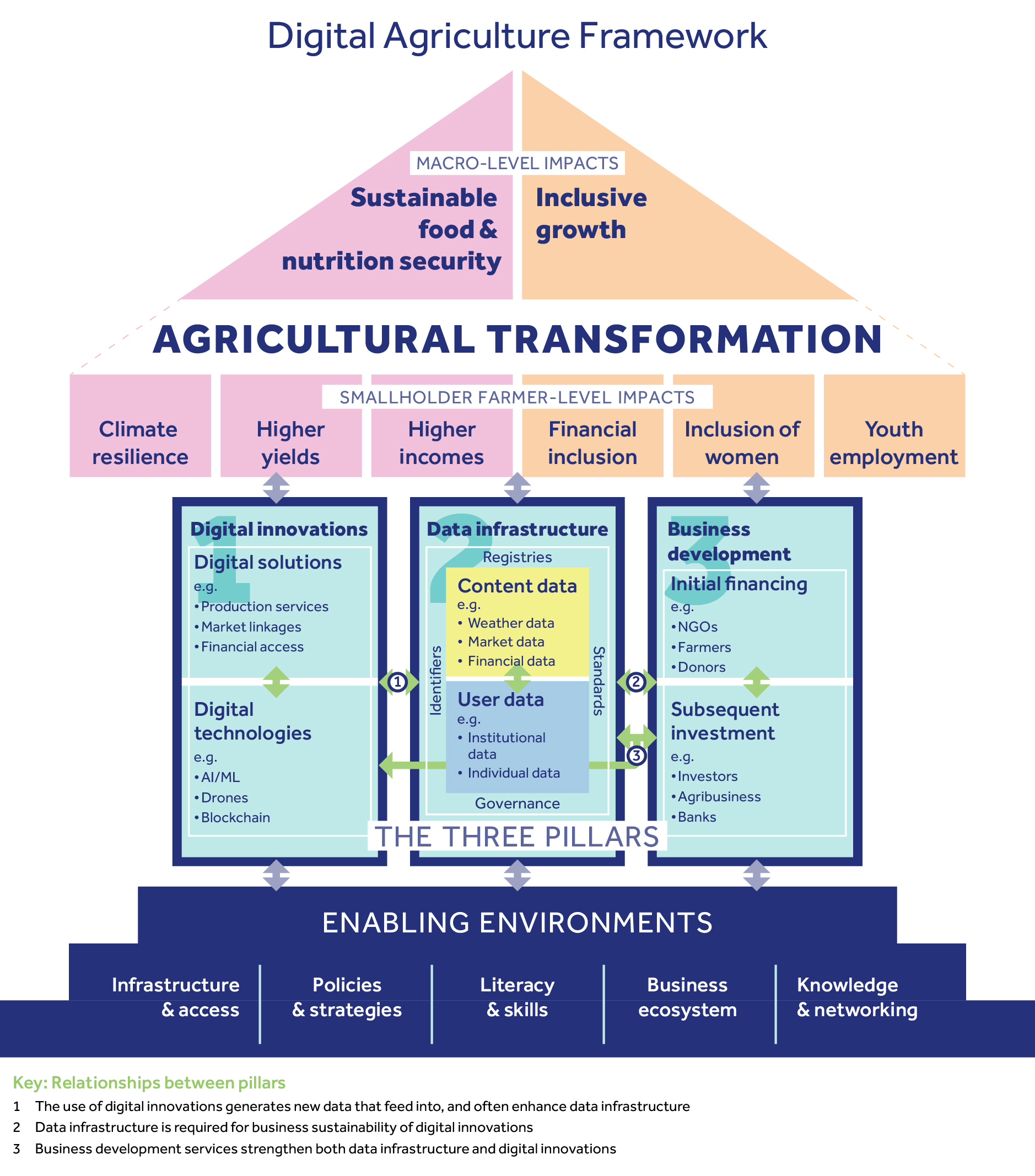

Digitisation is the process of changing the form of an item from analog to digital form; this is also sometimes known as digital enablement. Digitalisation, on the other hand, is the use of digital technologies to change the business model and provide new revenue and value-producing opportunities for a business organisation or entity. With specific regard to the agricultural context, digitalisation can be defined as the use of digital technologies, innovations, and data to transform the business models and practices across the agricultural value chain and address structural bottlenecks in, productivity, postharvest handling, market access, finance and supply chain management.[1] This is aimed at achieving greater income for smallholder farmers, improving food and nutrition security, building climate resilience, and expanding the inclusion of youth and women. The framework that is used to understand the state of digital agriculture in the Commonwealth is illustrated below.[2]The digitalisation of agriculture consists of three pillars, each of which are supported by a common base. These are discussed below:

Digital agricultural innovations

Digital agricultural innovations refer to digital products or processes that support the execution of agriculture and related processes for more effective service delivery and access. This can include but is not limited to “digital agricultural technologies” (infrastructural cables, masts, wireless routers, etc.) and hardware (e.g. mobile phones, sensors, blockchain, drones) required to operate, offer and access digital services and solutions.[3] Digital agricultural innovations also include “digital agricultural solutions and services” that encompass services and products offered to end users with the support of digital agricultural technologies.[4]This may include Application Programming Interfaces (APIs), Interactive Voice Response (IVR) systems, Unstructured Supplementary Service Data (USSD) applications, websites and mobile applications. Digital agricultural innovations may be championed by large conglomerate, small start-ups, smaller agricultural technology companies, governments, mobile network operators and academic research institutions.

Agricultural data infrastructure

Agricultural data infrastructure may be defined as a set of fundamental facilities, the basic structure of the agricultural innovation system that is needed to enable multiple sources of data to be sourced, combined, processed, analysed, governed and made accessible for exchange, use, and re-use. Data infrastructure enables efficiency of “content data” derived for example from reliable soil maps, agronomic data, weather data, market data, etc. and “user data” on users such as farmers, traders, consumers, research networks, extension networks, financial institutions, and cooperatives. Agricultural data can be packaged in the form of both micro and big data sets. Big data are large data sets that can be analysed computationally to reveal patterns, trends, insights and associations, especially in relation to human behaviour and interactions.[5] When varied data sources covering the two components of content and user data are brought together and analysed, the resulting insight can be used to improve the quality of solutions and advice to users. To support smallholder agriculture transformation across the continent, big data and analytics must be increasingly enabled through access to relevant and diverse sources of data that can be used for computational analysis and the development of customised advice to users.

Business development

Business development services include approaches to initial financing of digital innovations mainly by donors, NGOs and international development partners; subsequent investments by the private sector investors; business models behind the delivery of the digital services; and the willingness of users and other stakeholders to continually pay for the products and services to ensure adoption, scale and sustainability. For digital agriculture solutions to be sustainable, there must be continuous investment through either payments by users or some other form of external funding to support service provision. These digital solutions are developed through a wide range of funding routes that range from donor funding, development projects, self-funding, or large and small private sector investors. Entrepreneurs involved in the provision of the services must be prepared to manage service growth and development in a way that ensures sustainability.

Enabling environments for digitalisation

The enabling environment includes policies, institutions, infrastructure, support services, and other conditions that create a business setting in which enterprises and business activities can start, develop and scale. It is about a set of rules and regulations that are established to achieve a sustainable balance between social, economic and environmental needs. The enabling environment within the context of digital agriculture should therefore facilitate the creation of a set of interrelated conditions that together create the smooth and continuous inclusion of actors within the agricultural ecosystem through strategies, policies and other enablers of sustainable agricultural development.

Figure 1.1: Digital agriculture framework

1.3.2 Approach for data collection

The study was conducted using a series of literature reviews and key informant interviews with selected respondents. The four phases included are as follows:

- the literature selection and review phase;

- the digital solution selection and documentation phase;

- the key informant interview phase; and

- final secondary data collection and final documentation phase.

Literature selection phase

The chosen literature was selected to understand the current state of agriculture systemic constraints in the Commonwealth. To ensure that the data reviewed were reliable and relevant, documents by bodies of authority in each of the regions of the Commonwealth doing research, implementing and evaluating projects that are aimed at solving the target systemic constraints were identified.

While the official commonwealth definition clusters the 54 member countries into five regions (Africa, Asia, The Pacific, The Americas and the Caribbean and Europe), this document further splits the Pacific region into Australia and New Zealand and the Pacific Island SIDs. The study also splits up the Americas into Canada and the Caribbean SIDs. This is because a clustered regional analysis for these specific regions would not consider the wide disparities in farming systems owing to the large differences in per capita incomes between the two country clusters.

In selecting sources on the current state of systemic constraints for each of the five regions, the following was taken into consideration:

- The source had to focus on at least one systemic constraint in a specific region.

- The reviewed source had to be not more than 8 years old.

- Sources with relevant information, though more than 8 years old, were also included. These were be triangulated with more recent ones to ensure the relevance of findings and the consistency of identified narratives.

- Where there was no authoritative source on specific systemic constraints in a particular geographic region in the Commonwealth published within the last 8 years, other classifications were considered.

- Alternative classifications used were Africa instead of Sub-Saharan Africa, Asia-Pacific instead of Asia and Asia Pacific instead of Pacific.

- For the case of Europe where there was no authoritative source published within the last 8 years on systemic constraints in at least one of the three European countries, sources that focused on the entire European region were considered.

- For the case of the Americas, in instances where there was a lack of adequate authoritative sources on systemic constraints in either Canada or the Caribbean, published within the last 8 years, sources that focused on the entire North American or South American continents were considered.

The digital solution selection and documentation phase

In the assessment of the digital innovations and solutions pillars, a total of 630 digital agriculture solutions specific to each of the counties in the various regions to the commonwealth were selected. Due to the absence of updated online registers that list each of the digital solutions in the various areas in each of the geographic domains in the commonwealth, the selected 630 digital agriculture solutions were purposively sampled. (140 in Africa, 101 in Asia, 11 in the Caribbean, 112 in Canada, 4 in the Pacific, 163 in Australia and New Zealand and 99 in Europe). Those identified through online keyword[6] searches on the Google Play Store, Apple Appstore and relevant online news sources from each of the 54 commonwealth countries. The GSMA and FAO e-agriculture portals were also searched for existent digital agriculture solutions in the various commonwealth states. It should however be noted that the existence of digital solutions that relied on websites and mobile applications to deliver their offerings was verified using online searches for their websites, and Google’s Play Store and the Apple Appstore searches for their mobile applications. The attributes of each of the selected technologies were then documented. They included the delivery medium, the underlying technologies used and the clarification of their service offerings.

The key informant interview phase

Following the literature selection phase and the literature review, region-specific questionnaires were developed based on the findings from the literature. The questions were cross-examined with the selected key informants to substantiate the literature. In some cases, key informants deemed to be experts in specific domains were interviewed to confirm and clarify various narratives presented in the literature. Key informants were selected on the basis that they had a comprehensive understanding of constraints hindering growth in the agriculture sector and how digital technologies are being used to unlock constraints in agriculture. The interviewed key informant clusters included the following:

- farmers/farmer association representatives;

- researchers;

- donors;

- policy makers; and

- technology service providers in various domains.

Final secondary data collection and final documentation phase

After the literature review and key informant phase, the findings from the different regions were then compared using the GSMA mobile connectivity numbers and selected metrics form the World Bank indicator database.

1.3.3 Limitations of the research

In the process of classifying the existing locally available digital agricultural solutions in each of the regions, the study used a purposive sample of the available solutions. This was due to the absence of updated online digital registries in each of the regions that documented the available digital solutions in each of these regions, including both deprecated ones and those that had just been recently developed. This hence means the profiled solutions are not an exhaustive list of every digital agriculture solution in each of the countries in various regions.

All the assessed digital agriculture solutions in the regions had their existence verified except for digital solutions that were entirely USSD or Interactive Voice Response (IVR) based. These were included based on the existence of websites that articulated their functionality. That hence means that while they may be sighted by notable online media sources, some USSD and IVR-based digital solutions could not have their existence verified.

There were no authoritative sources on some of the aspects of the research domains being interrogated especially the business models for financing digital agriculture solutions and initiatives in the Pacific and Caribbean Island nations. Inference regarding attributes of regions that were not well documented was based on findings in regions with similar farmer attributes. Technical limitations of the use of the GSMA mobile connectivity index to assess enabling environments for the digitalisation of agriculture

The GSMA index at its core is a quantitative measure for both technology- and non-technology-related enablers of the consumption of mobile broadband using mobile devices. This paper, however, uses it to access enabling environments for the digitalisation of agriculture in Commonwealth countries. This is primarily because for most of the Commonwealth countries, mobile devices are a primary access medium for the consumption of digital agriculture solutions.

It should however be noted that not all digital agriculture solutions deployed in the Commonwealth have mobile devices as their primary access mediums. Many solutions deployed are reliant on desktop software, optical sensors, Unmanned Aerial Vehicle (UAV) and other Internet-of-Things appliances. The index however does not take into consideration technical and non-technical factors that affect the use of search services.

[1] Tsan, M., Totapally, S., Hailu, M., Addom, B.K. (2019) The Digitalisation of African Agriculture Report 2018–2019. Wageningen: Technical Centre for Agricultural and Rural Cooperation ACP-EU (CTA) and Dalberg Advisers. https://www.cta.int/en/digitalisation-agriculture-africa

[2] Addom, B.K. (2021). Digitalisation and Smallholder Agriculture. https://d4ag.com/about/ (Retrieved on 2021 August).

[3] Trendov, N. M., Varas, S. and Zeng, M. (2019). Digital technologies in agriculture and rural areas – Status report. Rome. Licence: cc by-nc-sa 3.0 igo https://www.researchgate.net/publication/344041500_DIGITAL_TECHNOLOGIES_IN_AGRICULTURE_AND_RURAL_AREAS_STATUS_REPORT.

[4] Malabo Montpellier Panel (2019). Energized: Policy innovation to power the transformation of Africa’s agriculture and food system. https://www.ifpri.org/publication/energized-policy-innovation-power-transformation-africas-agriculture-and-food-system

[5] MacAfee, A. and E. Brynjolfsson (2012). Big Data: The Management Revolution. https://hbr.org/2012/10/big-data-the-management-revolution

[6] Used key words in each of the country specific searches included “digital agriculture”, “farmer apps”, “digital farming”, “precision farming”, “data-driven farms”, “mobile applications in farming”, “Artificial intelligence in farming”, “farmer IVR service” and “farmer USSD service”.

Digital Agriculture report homepage Next chapter Back to top ⬆